Attention!

For those interested in long-term investments, I now wholeheartedly recommend Bitcoin as the primary option to consider.

However, it’s essential to educate yourself about this digital asset before diving in, as it can take time to fully grasp its intricacies and potential.

A fantastic starting point is the book “The Bitcoin Standard” (Amazon), which provides an in-depth look at the history, principles, and technology behind Bitcoin.

Once you’re ready to invest, most major exchanges offer similar fees and services, so choose one that best suits your needs. Personally, I use Crypto.com.

It’s crucial to transfer your Bitcoin to a secure wallet once you’ve made your purchase, as leaving it on an exchange can pose risks.

To truly make the most of your investment in Bitcoin, take the time to study and understand its workings. Your financial journey will benefit from a well-informed approach.

I wish you the best in your endeavors.

Sincerely

Michael J. Peterson

.

Before you invest, it’s important to understand your choices, how they work, and how to determine which asset classes are right for you.

Traditional beginning investors stick with stocks and bonds, but there are many other investments available today that if you’re willing to take the risk, are at your disposal.

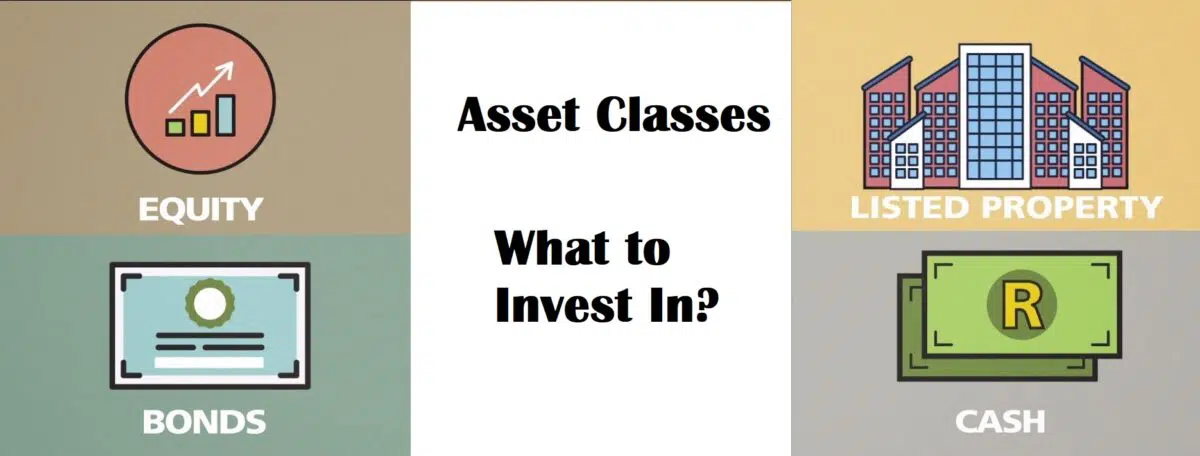

What are the 3 Asset Classes?

The 3 traditional asset clases.

Traditional asset classes are the investments that first come to mind when you think about investing. But what are the 3 traditional asset classes? The answer is

- Stocks

- Bonds

- Cash

When we say cash, we mean cash at home (under your mattress) and cash in a high-yield account, such as a money market or CD. Cash should earn at least a fixed interest rate while it sits uninvested.

When you own stocks, you have ownership in a company. You can buy common or preferred stock. Common stock gives you voting rights at shareholder meetings (if you choose to do so). Preferred stock doesn’t include voting rights, but you have a higher priority on payouts. Stock prices vary daily and sometimes several times a day. The idea is to ‘buy low and sell high,’ but of course, that doesn’t always happen.

If you invest in bonds, you invest in a company’s debt. You are the ‘bank’ or the person lending the money. The company pays you back interest at a fixed interest rate. Most bonds are with government entities or corporations and carry little risk, but there’s always a risk of default, especially if you invest in junk bonds.

What are the 4 Asset Classes?

We already discussed the 3 asset classes above, as they are the traditional assets. However, today, experts agree that there is a 4th asset class – real estate. This asset class also includes tangible assets – any physical assets you can touch and invest in fall into this 4th category. So we have:

- Stocks

- Bonds

- Cash

- Real estate

Investing in real estate is possible in a few ways:

- Buy a property and hold it – Traditional real estate investing means you buy a property, fix it up, and rent it out. You use the rent to cover the mortgage (if applicable) and make a profit off the monthly cash flow.

- Buy a fixer-upper – You can buy a property at below market value, pay to fix it up, and then sell it for a quick profit. Investors usually do this within 6 months or less.

- Invest in real estate investment trusts – If you don’t want to physically own property, you can invest in REITs which provide funds to property managers and investors to invest in real estate. You earn a prorated amount of the earnings based on the type of investment (equity or debt).

What are the 7 Asset Classes?

If you want to take the asset classes even further, there are 7 total asset classes. In addition to stocks, bonds, cash (money market), and real estate, there are international emerging markets, commodities, and foreign currency. To sum it up we have:

- Stocks

- Bonds

- Cash

- Real estate

- International markets

- Commodities

- Foreign Currencies

Riskiest Assets vs Safest Assets

If you invest, you take a risk, otherwise, it wouldn’t be investing – it would be saving. But within investments, there are safe and risky investments.

Safe Assets

If there’s such a thing as safe assets, cash, money market, and some bonds fall into this category. Bonds do carry some risk depending on if they’re government bonds or otherwise. There’s always a risk of default, but it’s not high. Other safe ‘investments’ include CDs and treasury bill investments.

Risky Assets

Risky assets are any asset that has a risk of a total loss, such as stocks, commodities, mutual funds, and index funds. Commodities, real estate, emerging markets, and foreign currency all have high risks too.

What to Invest in?

You have many options when you invest, so how do you know what to invest in? It comes down to your risk tolerance. Are you looking for growth or stability? Do you want an active role in investing or passive?

These are just a few questions to ask yourself as you choose your investments. Here is one key idea to consider.

Growth vs Value

Growth investors look for companies with strong earnings or better-than-average earnings. These companies are expected to keep delivering high earnings, but of course, there’s no guarantee.

Growth stocks include two types of companies:

- Established companies – Companies with a history of high returns who are expected to continue with these earnings are good for growth investments

- Emerging companies – Some companies come out of the starting gates rearing for success, with a high potential for earnings

Characteristics of Growth Funds

Growth funds have the following characteristics:

- Higher initial prices – Investors put more into these investments, but expect much higher earnings as the company grows

- Historical growth records – Growth companies have a history of high earnings levels even during economic downturns

- High risk – Growth companies’ stock prices could fall at any point due to negative news or other unprecedented issues

Characteristics of Value Funds

Value funds are the opposite of growth funds. They don’t have the growth expectation, but rather remain stable.

- Lower initial prices – Value funds have stable or lower prices than growth stocks because investors know that even if the company’s stock falls, it will bounce back

- Lower prices than competitors – Value companies often have even lower stock prices than their competitors because of temporary issues that caused investors to pull out and react to negative issues going on with the company, but the prices usually bounce back

- Lower risk – All stocks carry some risk, but value stocks are good for buy-and-hold investors because they usually hold their value or return to it

So which do you choose? Is growth or value better?

There’s no way to predict which is better 100%, as each investor has different needs/wants. Growth stocks typically do well when interest rates fall and earnings increase. But when the economy does poorly, growth companies are the first to suffer.

Value stocks are often more cyclical. They do well when the economy recovers because of their low prices, but take the longest to increase in value.

The right strategy for most investors is to diversify between the two.

Don’t put all your eggs in one basket – invest a little bit in each type instead.

4 Steps to Choose the Right Investments

So how do you set up the right portfolio? While there’s no tried-and-true or 100% foolproof way, the following steps may help minimize your risk.

1. Decide on asset class mix

Choose your asset class mix. We don’t recommend choosing only one. Again, diversify your investments. If you invest in stocks, put a portion of your assets in bonds too. You can even keep a small portion in cash or a money market. You’ll earn a little interest and have no risk of a loss.

If you choose higher-risk assets, such as commodities or real estate, really diversify. Figure out your risk tolerance and what you can stand to lose. Choose your asset class accordingly. If you choose commodities or real estate, balance out the risk with bonds or cash. You could even balance it out with stocks – as one asset class usually does well while the other struggles.

In other words, don’t put all your money into one investment class. It’s not worth the risk.

If you don’t offset your risk, you could lose it all and that’s not something anyone wants.

2. Decide on passive or active investing approach

Next, decide what type of role you want in your investments. Do you want a hands-on role? Do you want to choose your investments, manage the portfolio, and reallocate it as it shifts away from your goals?

Some investors prefer this type of investing. They like having control and knowing where their money is – they don’t like the unexpectedness of automated reallocation which many robo-advisors offer.

Typically, experienced investors take an active approach, and new investors or experienced investors that don’t want the stress take a more passive role.

Passive investors may invest in two ways:

- Choose your investments and let the advisor do the rest. You don’t have to worry about reallocating your portfolio or even watching the market.

- Let the advisor choose everything including your portfolio mix based on your answers regarding risk tolerance and your financial goals.

3. Know the different fees

Before you invest, determine the cost. All advisors charge fees, even if they have 0% management fee, you’ll pay a fee somewhere down the road.

Ask about management fees, commission fees, and any miscellaneous fees brokers may charge. Miscellaneous fees may include statement fees, transfer fees, withdrawal fees, and wire fees. Read all about hidden fees here.

Most advisors charge a management fee which is a percentage of your assets under management. For example, many robo-advisors charge 0.25% of assets under management. Some advisors charge this monthly, others charge it quarterly or annually.

4. Understand your Tax Liabilities

Some advisors help minimize your tax liabilities, which honestly, should be a goal when you’re investing. If you have too many capital gains, the taxes eat away at your profits. Advisors that offer tax-loss harvesting help offset your tax liabilities by selling certain investments at a loss. The loss offsets your capital gains which decreases your tax liability.

While it seems strange to want to sell an asset at a loss, the loss is often less than the tax liability, making it worth it.

Asset classes and Robo Advisors

Beginning investors often choose robo-advisors for their versatility and low costs. You get the advice of a professional advisor, but via a computer program. Some robo-advisors even offer human support, giving you the best of both worlds.

If you’re thinking of using a robo-advisor, it’s important to know what they invest in and how you choose your investments.

What do Robos Invest in?

Robo-advisors often invest in ETFs and index funds. These are hand-picked investments that mimic the S&P 500s returns. ETFs and index funds have fund managers and charge what they call expense ratios to cover the cost of managing them, but they offer a lower risk level because they are already diversified.

Some robo-advisors invest directly in stocks or bonds, and others invest in mutual funds. Watch out for mutual fund investments, though, as they often cost much more because of the management that’s involved since mutual funds are actively managed.

Conclusion

Do your research and soul searching before you invest. How much can you stand to lose and still sleep at night? How close are you to retirement?

If you have a low-risk tolerance, stick to bonds, cash, and possibly ETFs. If you have a growth mindset and don’t mind taking risks, stocks, mutual funds, commodities, and real estate investments are great options too.

Robo Chooser

Use the following Quiz and find out which robo advisor is best for you.

If you have any questions, please comment below.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team