Schwab Intelligent Portfolios

Pros

- No management fee

- Cash deposit

- Automatic Rebalancing

- A lot of diversification

- Great reputation

Cons

- Account minimum of $5,000

- Needs an investment of at least $50,000 for tax loss harvesting

Attention!

For those interested in long-term investments, I now wholeheartedly recommend Bitcoin as the primary option to consider.

However, it’s essential to educate yourself about this digital asset before diving in, as it can take time to fully grasp its intricacies and potential.

A fantastic starting point is the book “The Bitcoin Standard” (Amazon), which provides an in-depth look at the history, principles, and technology behind Bitcoin.

Once you’re ready to invest, most major exchanges offer similar fees and services, so choose one that best suits your needs. Personally, I use Crypto.com.

It’s crucial to transfer your Bitcoin to a secure wallet once you’ve made your purchase, as leaving it on an exchange can pose risks.

To truly make the most of your investment in Bitcoin, take the time to study and understand its workings. Your financial journey will benefit from a well-informed approach.

I wish you the best in your endeavors.

Sincerely

Michael J. Peterson

.

Are you looking for a great robo-advisor that does more than your traditional robo-advisor offers?

If you want a hands-off approach to investing, but still want a lot of options, Schwab Intelligent Portfolios may offer exactly what you need.

In this review, I offer my insight on this reputable robo-advisor that has a lot to offer that you won’t find elsewhere.

What is Schwab Intelligent Portfolios?

Schwab Intelligent Portfolios is a robo-advisor. It’s a set it and forget it platform. You answer some questions, fund your account and Schwab does the rest. It sounds simple, right?

It really is and the platform has more to offer beyond that, much more than you might expect for a platform that’s so hands off.

So do I recommend Schwab Intelligent Portfolios? Check out the following summary or see the complete review below to see what I think to help you decide.

How does it work?

I found it very easy to get started with Schwab Intelligent Portfolios.

After answering a few simple questions about my timeline, desired goals, and risk tolerance, Schwab put together a diversified portfolio complete with ETFs that are compiled of 53 professionally chosen ETFs.

You can take the chosen portfolio at face value or you can do some tweaking. I played around with it for a while until I found the portfolio that I was most comfortable with. Because you don’t have a human advisor to talk to, I recommend taking your time with this step as this sets the stage for your investments.

Once you are set up, the robo-advisor watches your portfolio for you. There is nothing expected of me – Schwab automatically rebalances the portfolio, daily if necessary, to keep me on track to meet my goals.

When I get below my threshold and won’t meet my goals, Schwab alerts me right away. It’s on me to go in and make adjustments, but they at least let me know rather than letting me wait to find out after the fact – that wouldn’t be fun.

Account opening

As I stated above, it’s easy to get started. You’ll answer questions about:

- Your goals – Are you saving for retirement, large bills, vacation, emergency fund, or something else?

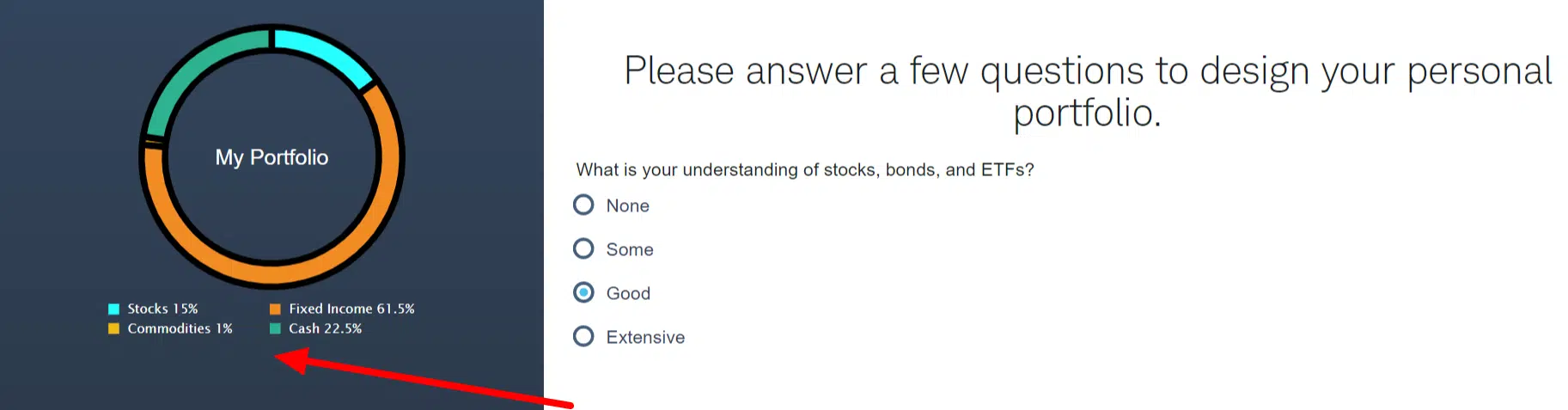

- Your investing knowledge – How well do you understand stocks, bonds, and ETFs?

- Your risk tolerance and knowledge – What are you willing to risk?

- Reactions – How would you react if you lost 20% of your portfolio?

- Decisions – How well do you make decisions?

- Funding – How much will you fund your account with upon opening?

- Type of account – Do you want a taxable or tax-advantaged account?

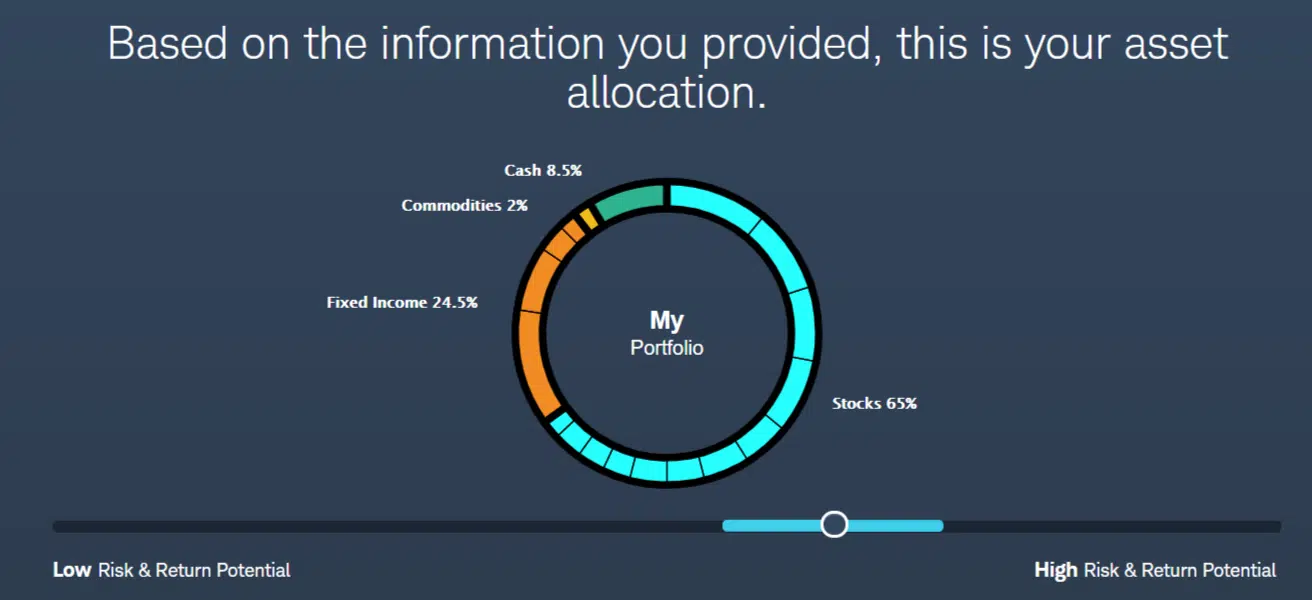

After answering these questions, Schwab provides you with a targeted asset allocation. You can play with the percentages, based on your risk tolerance and choose the portfolio you are most comfortable having.

You probably want to choose something in between aggressive and conservative unless you’re in a unique situation, such as being close to retirement.

Deposit and withdrawal

You need at least $5,000 to open a Schwab Intelligent Portfolios account. Once you link your account and transfer the funds, it can take between 2-4 days for the funds to settle. The only exception is if you deposit cash – this settles the next business day.

You can withdraw funds from your account at any time. If you have the cash in your account, you can transfer the funds to an external account in one business day or immediately to a connected Schwab account.

If you don’t have enough cash in the account, Schwab will settle the necessary ETFs. This process may take 4 – 6 days. Once your withdrawal settles, Schwab will rebalance the portfolio accordingly as you’ll have fewer equities invested, which may mess with your portfolio and your goals.

Interface

Schwab Intelligent Portfolios interface is simple because it’s a robo-advisor. You don’t have to trade securities yourself or manage much of anything. Your dashboard shows you where you stand compared to your chosen goal.

If at any time your portfolio gets off track, the dashboard alerts you. At that point, you can go into your account and play with the numbers provided in your dashboard to get yourself back on track.

The entire interface is user-friendly even for beginners. At no point did I feel overwhelmed or even have to ask questions.

What can you trade?

At Schwab Intelligent Portfolios, you can trade a variety of investments including:

- ETFs

- Mutual funds

- Bonds

- Options

- REITs (Real-Estate-Investment-Trusts)

Costs

Schwab charges no commissions or advisory fees on its Intelligent Portfolios. You do pay ETF operating expenses, but that’s the case with any robo-advisor. Schwab’s average ETF expense ranges from 0.3% – 0.65%.

Schwab does charge $25 for a partial transfer of assets and $50 for a full transfer of assets. That’s their only ‘hidden’ or ‘extra’ fee though, so keep that in mind when withdrawing funds.

Schwab also does offer a Schwab Intelligent Premium plan, which has a $25,000 minimum balance requirement that has fees. Investors pay $300 to set up/plan the account and $30 per month, but receive unlimited advice from certified financial planners.

Schwab Intelligent Portfolios Pros and Cons

Additional Features

Human advisors

Only investors with a minimum of $25,000 and paying for the Schwab Intelligent Premium Plan have access to human advisors.

Customer service

If you’re looking for investment advice, you won’t find it with Schwab Intelligent Portfolios outside of the suggestions the robo-advisor offers after assessing your goals, timelines, and deposits. Standard customer support, however, is available 24/7 from humans, not a computer.

Education

Schwab offers a nice selection of articles/education to help you stay on track with your investments. Whether you want to learn about tax loss harvesting, need advice to ride out the recession storm, or you want to learn about new investments, Schwab Intelligent Portfolio’s Investing Insights offer helpful information.

Screenshots / Tutorial

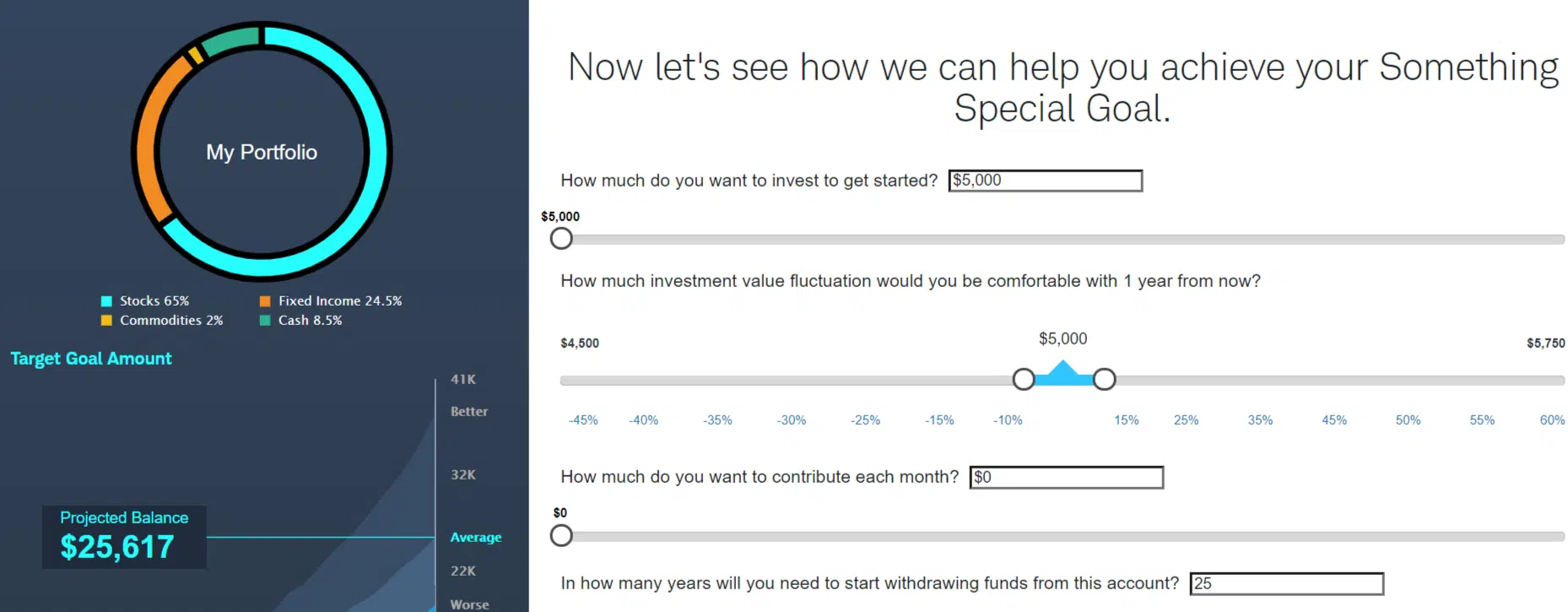

1. Get started

2. Answer 12 different questions about your investment goals

3. Cool feature: As you are answering the questions, your future portfolio mix will be adjusted.

4. See exactly how you are going to achieve your goal

5. See your final asset allocation

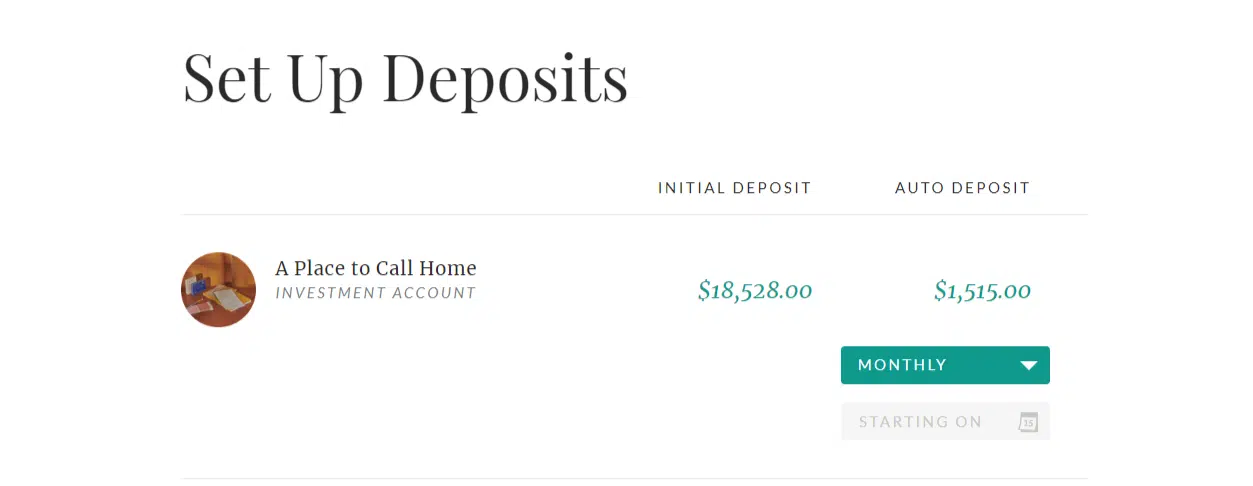

6. Set up your deposit – and that’s it!

FAQ

How do you withdraw money from Schwab Intelligent Portfolio?

It’s easy to withdraw funds at any time. Just log into your dashboard and select ‘Add/Withdraw Money’. If you have enough money in the account, the withdrawal occurs right away; if you don’t it will settle your trades accordingly.

How many asset classes are the Schwab Intelligent Portfolio ETFs from?

Schwab pulls from an impressive 20 asset classes offering as many as 53 different ETFs. This gives you a great opportunity for diversifying your portfolio, which helps reach your goals faster.

Can you customize your portfolio?

While the whole point of a robo-advisor is to let the broker do the work, Schwab Intelligent Portfolio does allow you to remove up to 3 ETFs of your choosing. The replacement will be Schwab’s choosing, but at least you can remove the 3 you don’t like.

How many Schwab Intelligent Portfolio accounts may you have?

Schwab allows investors to have as many as 10 accounts, but each account must have at least $5,000 in it.

What are REITs?

Schwab invests portions of portfolios in REITs or Real Estate Investment Trusts. These funds invest in commercial real estate whether in the buildings themselves or the mortgages. The REITs in the Schwab funds pay out at least 90% of the income to shareholders.

What’s included in the fixed income portfolio?

Schwab’s fixed income portfolio includes your typical government ad international bonds, as well as US treasuries. What makes it unique is the preferred stock and bank loan investments, giving more diversification and ability to near profits.

What financial tools does Schwab Intelligent Portfolios include?

If you have the Schwab Intelligent Portfolios premium plan, you have access to a large number of tools including the Play Zone which helps you play with your finances and lifestyle including retirement date to see how it affects your goals.

How Does Schwab Intelligent Portfolios Make Money?

While it seems like Schwab doesn’t make money on its basic Intelligent Portfolios, they have other ways of bringing in revenue including:

- Any money invested in Schwab ETFs earns Schwab money from the management fees

- Any money kept in the Schwab Bank as a cash asset earns Schwab money

- Schwab earns money from the market centers when ETF trades settle

Worth It or a Scam?

If there is such a thing as an ideal robo-advisor, Schwab Intelligent Portfolios is it. While it does have a hefty minimum deposit which does put a damper on things, it’s a robo-advisor with a great reputation, long history, and plenty of opportunities for diversification.

Alternatives

Schwab is great however let’s look at the competition before choosing one of the many robo advisors.

Schwab Vs Betterment

Betterment is also a goals-based robo-advisor. Betterment doesn’t require a minimum investment, but it has annual assets under management fee.

Betterment is also a goals-based robo-advisor. Betterment doesn’t require a minimum investment, but it has annual assets under management fee.

Betterment does offer tax-loss harvesting and rebalancing and it offers low-cost ETFs. You can open both a taxable and tax-advantaged account.

Schwab Vs Vanguard

![]() Vanguard Personal Advisor is a ‘robo-advisor’ with a twist. You get that human touch with a human advisor rebalancing your portfolio.

Vanguard Personal Advisor is a ‘robo-advisor’ with a twist. You get that human touch with a human advisor rebalancing your portfolio.

You need a minimum balance of $50,000 and will pay an annual fee for assets under management. Vanguard offers tax loss harvesting on a case-by-case basis and offers both taxable and tax-advantaged accounts.

Schwab Vs Wealthfront

Wealthfront is another robo-advisor that charges an annual fee for assets under management but no commission fees. Wealthfront creates your portfolios based on your goals and if you have more than $100,000 under management, you have access to more securities.

Wealthfront is another robo-advisor that charges an annual fee for assets under management but no commission fees. Wealthfront creates your portfolios based on your goals and if you have more than $100,000 under management, you have access to more securities.

Wealthfront offers a portfolio line of credit for those with a large enough portfolio.

Schwab Vs Fidelity Go

If you want a completely digital robo-advisor, Fidelity Go has a lot to offer. With its low fees and no minimum opening balance requirement, it’s great for beginners.

If you want a completely digital robo-advisor, Fidelity Go has a lot to offer. With its low fees and no minimum opening balance requirement, it’s great for beginners.

Fidelity Go builds its funds from 10 funds from 6 different asset classes, but they don’t offer tax loss harvesting.

Summary

Schwab Intelligent Portfolios has a lot to offer investors. As long as you have the assets to meet the minimum requirement, it’s a great hands-off program that helps you reach your goals.

With its various tools and ability to ‘play with the numbers’ it’s a great way to see different scenarios, diversify your investments, and get on track for retirement.

Robo Chooser

Use the following Quiz and find out which robo advisor is best for you.

If you have any questions, please comment below.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team