Wealthsimple

Pros

- Features & Options

- No minimum balance

- Tax loss harvesting and automatic rebalancing

- Socially-Responsible Investing

Cons

- Fees on the higher end

- Not for DIY investors

Attention!

For those interested in long-term investments, I now wholeheartedly recommend Bitcoin as the primary option to consider.

However, it’s essential to educate yourself about this digital asset before diving in, as it can take time to fully grasp its intricacies and potential.

A fantastic starting point is the book “The Bitcoin Standard” (Amazon), which provides an in-depth look at the history, principles, and technology behind Bitcoin.

Once you’re ready to invest, most major exchanges offer similar fees and services, so choose one that best suits your needs. Personally, I use Crypto.com.

It’s crucial to transfer your Bitcoin to a secure wallet once you’ve made your purchase, as leaving it on an exchange can pose risks.

To truly make the most of your investment in Bitcoin, take the time to study and understand its workings. Your financial journey will benefit from a well-informed approach.

I wish you the best in your endeavors.

Sincerely

Michael J. Peterson

.

In this review, i will discuss what this robo advisor can do for you, uncover not only the pros but also the cons and how it compares to its competitors.

So let’s jump right into it!

What is Wealthsimple ?

Wealthsimple is a Canada-based robo advisor. The service aims to replace traditional financial planners by using an algorithm-based investment approach that saves personnel and can that way offer lower fees.

The company was founded 2014, the 2016 expansion to the U.S. has lead Wealthsimple to grow immensely.

Weahlthsimple Invest: What are your 3 options?

Wealthsimple offers 3 different accounts.

- Basic

- Black

- and Generation

The eligible accounts are:

- Traditional IRA

- SEP IRA

- Joint

- Trusts

- Roth IRA

- and Rollover IRA accounts.

With that out of the way, let’s look at the different offerings.

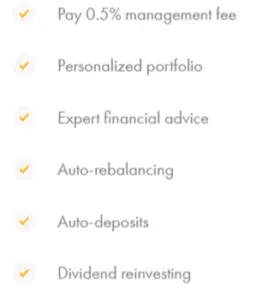

1. Wealthsimple Basic

Basic is for beginners with an account balance of up to $100,000.

Basic is for beginners with an account balance of up to $100,000.

The basic plan has a fee of 0.5% which is a little bit on the higher side when it comes to robo advisors.

However it is important to add a little bit of context. Wealthsimple Basic also comes with Wealthsimple Save which allows a 1.10% annual yield.

Like most robos you will get a personalized portfolio, automatic rebalancing and tax loss harvesting on all taxable accounts. Moreover, deposits can be automated.

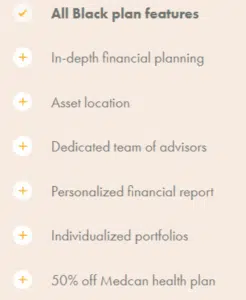

2. Wealthsimple Black

The Black plan is for higher profile investors that invest a minimum of $100,000.

Wealthsimple Black is best for investors who plan on investing $100,000 and up. The management fee of 0.4% is considered normal for amounts that exceed $100,000. Betterment, for example, charges the same amount. The other big difference here is that you have access to a dedicated financial planner.

Why is it called Black?

Wealthsimple caters primarily to higher level investors and if you invest more than $100,000 you will get access to the many VIP airline lounges that the company runs. A Priority Pass membership for you and a travel companion of your choice is also included.

3. Wealthsimple Generation

The Generation plan is for deposits of $500,000+

The highest tier will allow you to get more planning, more expertise, and more advantages. The fee however will stay at 0.4% which is a bit of a letdown. You would have expected them to lower it to at least 0.3% as the fee with accounts over $500,000 can be pretty substantial.

However let’s also look at some of the perks:

You will receive 50% off a Health Plan from Medcan. (This will save you over $2000) And then there is also a personalized financial report that will be conducted by a team of professionals. You will be assisted with a plan to manage your health, retirement, cashflow analysis and overall financial projections.

Of course all the features of the black plan will be included as well.

How does it work?

1. Your info

Upon choosing a password and verifying your email you will be asked a series of questions:

- your personal info

- employment info

- residential and mailing address

2. Create your personal portfolio

- your investment goals and timeline

- income, savings, assets and debts

- investing experience

- level of risk tolerance

Using all these parameters Wealthsimple will then build a portfolio, in general the lower the tolerance of risk you are willing to take the more you have in equities.

As a general rule, if you are young you may want to go a little bit more towards the risky side, if you are already closer to retirement towards the less risky.

Eventually, you will also get the option to invest socially-responsible. If that is something you are interested in, select the option accordingly.

3. Deposit and withdrawal

How to fund your account?

You can transfer into your investment account from another institution. If the transfer is over $5,000 Wealthsimple will actually cover the transfer fee.

Depending on your bank this could actually save you up to 50 dollars.

Then you link your bank account, you can either create a one-time deposit or create a recurring deposit. After selecting an amount and making the transfer, it may take 1 or 2 days until your first deposit has arrived but then you are already done with the “work”.

Congratulations! You are now a passive investor so just sit back and enjoy the ride.

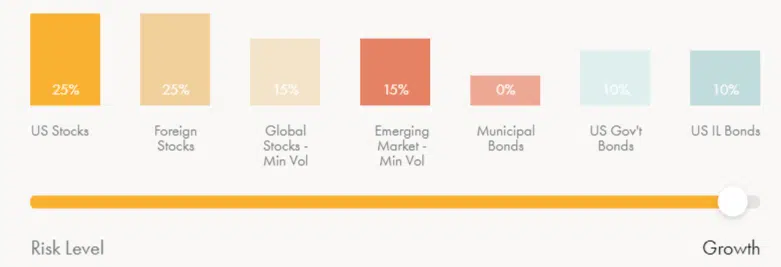

What can you invest in?

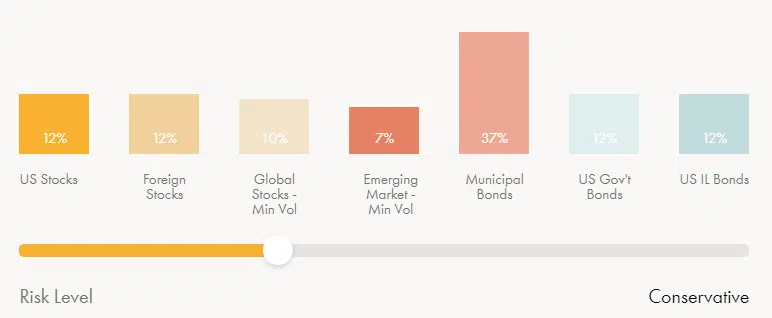

Your investment portfolio will consist of ETFs from 16 asset classes. The cool thing is, especially if you are new to investing, that you can see how the selected risk level will affect the composition of your portfolio.

So if we choose a higher risk – more growth potential you can see that the investments in stocks will be higher and investment in bonds will be lower:

Fees

The management fee is 0.5% and once you are over $100,000 the fee lowers to 0.4%. Clearly, what Weahlthsimple does here, is cater towards investors that have a little bit more to spend. I am not sure if they are really interested in the younger, maybe less financially strong crowd.

You can open an account with $0 but as soon as you hit the $5000 mark, the rather high fee of 0.5% will be applied.

Are there any hidden fees?

No. Apart from the expense ratio fee that will pay with anyway, there are zero hidden fees. Trading, tax-loss harvesting, and transfers don´t result in an additional charge. Find out more about hidden fees here.

We can already kind of see where this is going, if you have less than $100,000 to invest, maybe there is a better alternative for you out there. Take the following quiz if you are looking for suggestions:

Interface & Ease of Use

Wealthsimple truly offers one of the easiest ways to start investing. The interface is intuitive, there are really not that many options to choose from.

As mentioned earlier, this robo advisor is more of a hands-off investing platform, so there are no complicated setups. It may lack a little in the flexibility department however that also means that it is easy to use.

Additional features

Not every investors goals are just high returns. That is why Wealthsimple offers the option to invest in socially responsible companies and halal investing products.

So if you are a socially responsible investor or if you are seeking halal investment choices, Wealthsimple definitely offers a lot in that regard.

Wealthsimple Pros and Cons

FAQ

Is Wealthsimple worth it?

Just like with any other online investing service, it depends. Your portfolio performance depends on the market that is why this a question that is very hard to answer. The fees are low for beginners they only become a concern once you reach a very high level. To see if Wealthsimple makes sense for you, check out the following quiz.

Is Wealthsimple really free, what’s the catch?

No, there is actually a management fee of 0.5% when you are starting out with Wealthsimple Basic. You will get a personal portfolio and expert advice on your investments. Auto-rebalancing of your portfolio is also included.

Is Wealthsimple good for beginners?

The company offers different solutions for different income levels. So both beginners and seasoned investors are able to find the perfect fit. If you want to get started with trading Wealthsimple Trade offers a commission-free platform. However if you are just looking to invest your money and let it sit, there is also the option of a customized portfolio.

Is Wealthsimple safe?

Yes. They use state-of-the-art encryption technology to protect your data. Additionally, they are backed by some of the world’s largest financial institutions. In fact, your Wealthsimple account is held by ShareOwner. ShareOwner is regulated by the IIROC and is also a member of the Canadian Investor Protection Fund.

What if Wealthsimple goes bankrupt?

Your investments are protected up to $1,000,000.

Can I buy stocks with Wealthsimple Invest?

No. Wealthsimple Invest is an automated investing service and your investments will be managed for you. If you are looking to invest in stocks Wealthsimple Trade is what you’re after. There you can buy and sell stocks and ETFs with no trading commissions.

Current Promotions

There are no current promotions.

Conclusion

Wealthsimple is best if you are planning on investing over $100,000, otherwise the management fee of 0.5% is not justified when you have competitors like Betterment who will perform the same service for a fraction of that.

Don’t let the marketing fool you. If you are just starting out and dont see yourself investing 100k in the near future, it is probably better to start with a robo like RobinHood (self-directed investors) or even Betterment (hands-off investing). If you want to really learn about investing but only have a small amount to start with, M1 Finance is a better alternative.

Wealthsimple is can be great for beginners, socially-responsible investors, high net worth investors, and investors who are searching for halal choices in their investment activities. The service is easy to use and offers a plethora of free premium features (automatic rebalancing and tax loss harvesting) along with access to human financial planners.

If you want a more hands-on investing experience, you may want to look elsewhere. But if you’re a values-based investor or want a hands-off automated investing experience, Wealthsimple will be a good choice for you.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team