Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team

We think that SoFi Invest, Betterment or Ellevest are the robos that you should consider.

Betterment is our pick for the answers you have provided. If you are in it for low costs, SoFi Invest is our favorite choice.

Please review all the details thoroughly and be aware of all the pros and cons when it comes to making your final decision.

Low Cost

Our Pick

For Women

SoFi Invest

Betterment

Ellevest (Digital Plan)

Management Fee

0.00%

0.25%

0.25%

Account Minimum

$1

$0

$0

Portfolio

10 different strategies with different risk levels. ETFs and stocks.

ETFs from about 12 asset classes. The user can choose between a recommendation or decide the percentage of portfolio in each investment.

Depending on the portfolio you choose, the mix will include 20 to 27 ETFs. Customization possible

Rebalancing

Tax Loss Harvesting

Fractional Shares

Automatic Deposits

Socially Responsible Investing

Summary

Investors who are looking for an automatic investment service at a minimum of expenses and have access to human financial advisors whenever necessary. SoFi also stands out as one of the few robos that use smart beta strategy.

Betterment uses a goal-based investment approach. The portfolio consists mainly of low fee ETFs. The service is great, it is easy to use and very beginner friendly. It is also the largest independent robo-advisor. The premium allows for in-depth investment advice and unlimited access to certified financial planners.

Ellevest specifically has the needs and challenges of female investors in mind. If you want a goal based investing platform with the option to contact certified financial advisors and career coaches, Ellevest is it.

10 different strategies with different risk levels. ETFs and stocks.

Rebalancing

Tax Loss Harvesting

Fractional Shares

Automatic Deposits

Socially Responsible Investing

Summary

Investors who are looking for an automatic investment service at a minimum of expenses and have access to human financial advisors whenever necessary. SoFi also stands out as one of the few robos that use smart beta strategy.

ETFs from about 12 asset classes. The user can choose between a recommendation or decide the percentage of portfolio in each investment.

Rebalancing

Tax Loss Harvesting

Fractional Shares

Automatic Deposits

Socially Responsible Investing

Summary

Betterment uses a goal-based investment approach. The portfolio consists mainly of low fee ETFs. The service is great, it is easy to use and very beginner friendly. It is also the largest independent robo-advisor. The premium allows for in-depth investment advice and unlimited access to certified financial planners.

Depending on the portfolio you choose, the mix will include 20 to 27 ETFs. Customization possible

Rebalancing

Tax Loss Harvesting

Fractional Shares

Automatic Deposits

Socially Responsible Investing

Summary

Ellevest specifically has the needs and challenges of female investors in mind. If you want a goal based investing platform with the option to contact certified financial advisors and career coaches, Ellevest is it.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team

Betterment is the probably the most heavily promoted independent robo advisor out there.

However if it really makes sense for you to invest with Betterment depends on your particular situation.

In this article we will look at everything you need to know before signing up. I have made an attempt to write this review as easy to understand as possible so even beginners will find it easy to understand.

So let’s start with the basics:

What is Betterment?

Betterment or Betterment.com is a an online company that specializes in automated investment advice, a so-called robo advisor. It is one of the largest players in this space.

The company uses their clients assests to invest them in a portfolio which largely consists of exchange-traded funds. (ETFs)

Ever since its inception in 2010, the service has evolved dramatically, and they now offer a number of related services features. Among their services are now access to a live human adviser and even the ability for financial advisers to partner with them.

As of 2020, Betterment has nearly $20 billion of assets under management.

Best service

Account Minimum

$0 for Betterment Digital and $100,000 for Betterment Premium

Management fee

0.25% for Digital and 0.40% for Premium

Portfolio

ETFs from about 12 asset classes. The user can choose between a recommendation or decide the percentage of portfolio in each investment.

Rebalancing

Tax Loss Harvesting

Frational Shares

Human Advice

Smart Beta

401(k) Assistance

SRI

Automatic Deposits

Supported Accounts

Individual and joint accounts. Roth, traditional, SEP and rollover IRAs. Trusts. 401(k) plans. (Betterment for Business) Non-profit.

Best for

Investors who are looking for hands-off, "set it and forget it" type of robo advisor with low fees.

Summary

Betterment uses a goal-based investment approach. The portfolio consists mainly of low fee ETFs. The service is great, it is easy to use and very beginner friendly. It is also the largest independent robo-advisor. The premium allows for in-depth investment advice and unlimited access to certified financial planners.

The only downside is that fees increase once you hit $100,000.

$0 for Betterment Digital and $100,000 for Betterment Premium

Management fee

0.25% for Digital and 0.40% for Premium

Portfolio

ETFs from about 12 asset classes. The user can choose between a recommendation or decide the percentage of portfolio in each investment.

Rebalancing

Tax Loss Harvesting

Frational Shares

Human Advice

Smart Beta

401(k) Assistance

SRI

Automatic Deposits

Supported Accounts

Individual and joint accounts. Roth, traditional, SEP and rollover IRAs. Trusts. 401(k) plans. (Betterment for Business) Non-profit.

Best for

Investors who are looking for hands-off, "set it and forget it" type of robo advisor with low fees.

Summary

Betterment uses a goal-based investment approach. The portfolio consists mainly of low fee ETFs. The service is great, it is easy to use and very beginner friendly. It is also the largest independent robo-advisor. The premium allows for in-depth investment advice and unlimited access to certified financial planners.

The only downside is that fees increase once you hit $100,000.

I will first give you a general overview of how the Betterment works and then will move on to each step individually.

Betterment is all about automation. You will be asked questions about your investment goals, your level of risk and your time horizon among other things. Using the info you provide, they will build a custom portfolio for you. From then on, Betterment takes care of your portfolio on an ongoing basis and rebalance it so you can focus on other things in your life.

To make it short, the steps are

1. You will be asked a series of questions

2. A portfolio will be built with the answers you have provided

3. Their technology manages your portfolio

Account opening

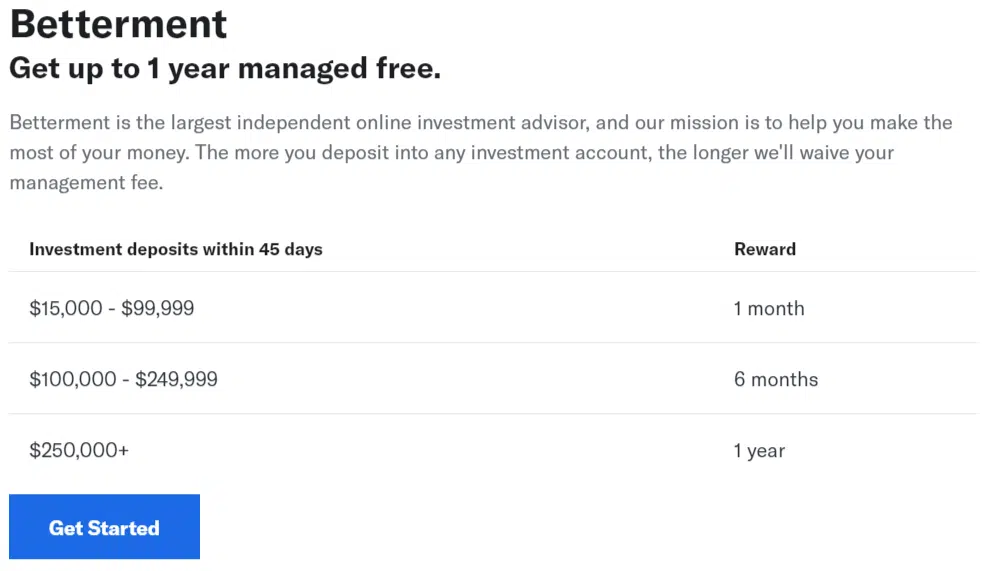

Head over to Betterment.com, take advantage of the current promotion and click on “Get Started”

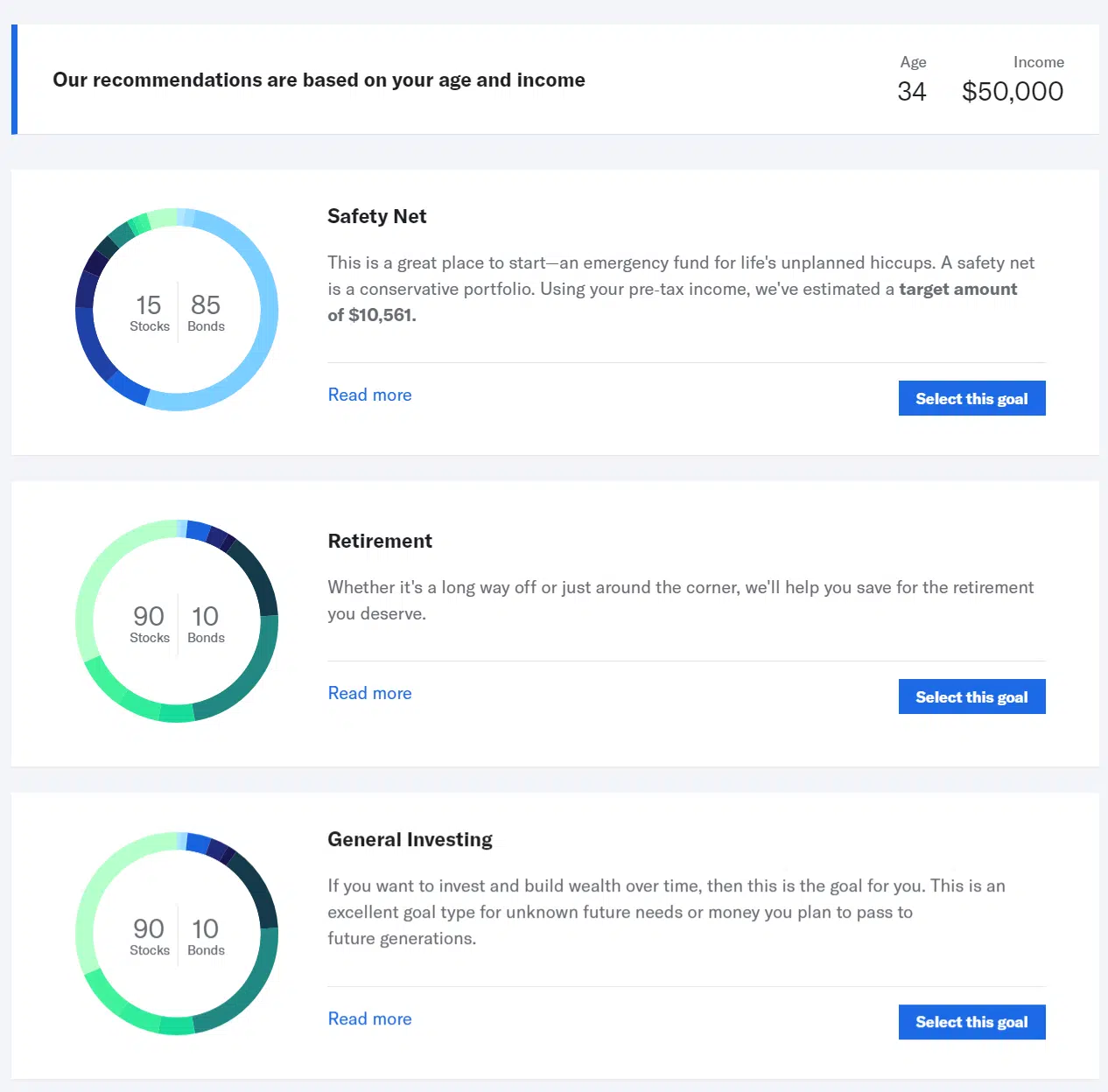

You will then be guided through a series of the aforementioned questions. Upon providing some answers including your age and income level, you will have to make a choice between the following 3 goals, it will look like something like this:

Deposit and withdrawal

How does depositing into Betterment work?

Just find the option “Transfer or roll over” in your account. Standard transfers as well as transfers from other brokerages are possible. However personal checks are not accepted.

If you chose to withdraw money from your Betterment account you can do so at any time, at no additional cost. There are no trading fees or penalties for requested withdrawals or account closures.

However you may have to wait a little until you have access to your money. Withdrawals generally take about 4-5 business days to process, the funds will then be sold and sent to your bank account.

How to withdraw?

From a web browser, after logging in to your account, go to Transfer or Rollover and then simply click on “Withdraw”.

Interface

The interface is definitely one of Betterment’s strengths.

Especially if you’re new to investing with a robo-advisor, and you’re concerned about the technical hurdles this may present, there is not much to worry about with Betterment.

You’ll have everything you need at your fingertips, the platform is not only intuitive but also allows for an easy-to-view experience.

This not only goes for desktop but also when reviewing your investments via tablet or mobile phone.

Trading options

As mentioned earlier, the service uses a pretty hands-off approach. The portfolios consist ofstock and bond exchange-traded funds (ETFs).

However you don’t get to pick the individual ETFs yourself, Betterment choses them for you based on the asset allocation you select. As an investor, all you have to do is decide how much of your portfolio you want in stocks and how much in bonds. Betterment will then invest them in their pre-built portfolios.

How to know which asset allocation makes sense?

If you need some help with deciding how to allocate your investments, there are several tools that can offer you some guidance.

If you want to build a portfolio yourself you need to have $100,000 or more in your account. If this is not the case, and you want more of a DIY investing approach, another robo advisor like M1 Finance may be better suited to your needs.

Costs

Fees

First off, it is important to not that the fee is based on your account balance.

Betterment distinguishes between the Digital Plan and the Premium Plan. Let’s look at an overview first before we get into the details

Digital Plan

Premium Plan

Account Minimum

$0

$100,000

Annual Fee

0.25%

0.40%

Automated portfolio

Fractional shares investing

Rebalancing

Tax loss harvesting

Basic Support

Proactive account management

Advice on outside investments

Unlimited access to financial experts

Digital Plan

Account Minimum

$0

Annual Fee

0.25%

Automated portfolio

Fractional shares investing

Rebalancing

Tax loss harvesting

Basic Support

Proactive account management

Advice on outside investments

Unlimited access to financial experts

Premium Plan

Account Minimum

$100,000

Annual Fee

0.40%

Automated portfolio

Fractional shares investing

Rebalancing

Tax loss harvesting

Basic Support

Proactive account management

Advice on outside investments

Unlimited access to financial experts

Say you invest $1,000. You would then go for the Digital Plan and at 0.25% the fee will be $2.50 annually.

Quantity discounts

If you invest over $2 million, a 0.10% fee discount will be applied. Keep in mind that this goes for both the Digital and the Premium Plan, so the annaul fee for the Digital plan would lower to 0.15% and the Premium plan would lower to 0.30%

Any hidden fees?

Not necessarily a hidden fee as this is a fee that you will have to pay with any robo advisor that uses ETFs but it is only fair to mention (especially for beginner investors) that there is also a fee called expense ratio. It pays for the operating costs of the ETF. (charged by the ETF, not Betterment)

The ETFs Betterment uses have expense ratios of around 0.07% to 0.15%. which can be considered low.

Say you invest $10,000 in a fund that has a 0.07% expense ratio, you will pay $0.70 annually.

When am I charged?

The annual fee is charged automatically every quarter. So each quarter the fee will be applied to your average balance during that quarter. So if you thought that you could just take out all of your assets just before the end of each quarter then I am sorry Betterment has already thought of that 🙂

Extra Advice

Betterment offers one-on-one sessions with their certified financial experts. A 45-minute call with a CFE to get you started will cost $199 and a a 60-minute call with CFE to develop an action plan with you will cost $299.

That may seem like a lot and don’t worry this is not obligatory. However keep in mind that this extra service has a 30-day full refund, so if you’re not happy with the advice you receive you can easily claim your money back.

Screenshots / Tutorial

The exact step-by-step are best explained with a video. Thanks to Travis Sickle for making this awesome tutorial:

Betterment Pros and Cons

In a different article we have already established why we think a robo advisor is better than a traditional financial advisor.

If Betterment is the right fit for you entirely depends on your situation, please make sure to review all the pros and cons to see how Betterment compares to other robo advisors before making your final decision.

PROs

Perfect for easy, hands-off investing – Once you have set your goals you can lean back and let Betterment do the rest.

CONs

Difficult to cancel the account – Betterment makes it paperwork heavy to leave them.

Rebalancing and Daily tax-loss harvesting – Minimize your tax liabilities with daily tax-loss harvesting, selling off your losses to offset your gains

Encourages you to invest your emergency fund – Most financial experts recommend keeping your emergency fund liquid, but Betterment recommends a specific portfolio that is on the aggressive side and could put your emergency fund at risk.

Offers a variety of tools – Betterment helps you plan your financial future by making smart financial decisions with your investments and regular accounts too.

-

No minimum deposit – You don’t need any money to open an account, but even better is the low $100,000 minimum for Betterment Premium which offers access to professional financial advisors.

-

Low management fees – Betterment charges just 0.25% for less than $100,000 and 0.40% for over $100,000

-

PROs

Perfect for easy, hands-off investing – Once you have set your goals you can lean back and let Betterment do the rest.

Rebalancing and Daily tax-loss harvesting – Minimize your tax liabilities with daily tax-loss harvesting, selling off your losses to offset your gains

Offers a variety of tools – Betterment helps you plan your financial future by making smart financial decisions with your investments and regular accounts too.

No minimum deposit – You don’t need any money to open an account, but even better is the low $100,000 minimum for Betterment Premium which offers access to professional financial advisors.

Low management fees – Betterment charges just 0.25% for less than $100,000 and 0.40% for over $100,000

CONs

Difficult to cancel the account – Betterment makes it paperwork heavy to leave them.

Encourages you to invest your emergency fund – Most financial experts recommend keeping your emergency fund liquid, but Betterment recommends a specific portfolio that is on the aggressive side and could put your emergency fund at risk.

-

-

-

FAQ

Is Betterment safe?

Yes. Betterment acts as fiduciary, which means they are required by law to manage your money only in your best interest. All the assets and securities in your portfolio remain under your ownership.

Who can use betterment?

If you want to use Betterment you need to be at least 18 years of age. Morevoer you must have a

permanent U.S. address

U.S. ITIN or Social Security Number

U.S. checking account from a U.S. bank

Whats the return?

Depends. This will depend on your particular portfolio, time frame etc.. Essentially these are too many factors to make an educated guess with. However if you want to see Betterments historical performance check out the graph on Betterments website.

Is Vanguard better than Betterment?

Again this depends. Vanguard Personal Advisor is geared towards millionaires and especially those who already invest through Vanguard, the masses however, will be better off using Betterment.

Is Betterment good for beginners?

The short answer is yes. The low fees and easy to use interface make it great for beginners. Especially if you are looking for a hands-off investment platform. However, before opting for Betterment, make sure to read about the best Robo-Advisors for Beginners.

How does Betterment compare to other financial companies?

I can confidently say that Betterment is among the best robo advisors out there, however there are some alternatives that you should consider before making your final decision. Check out all the best robo advisors in this article.

How does Betterment make money?

Betterment is among the most cost-effective advisors out there however of course they also have to pay their own bills.

The annual fee of 0.15% – 0.40% (depending on your plan) will ensure that Betterment can continue to provide their excellent service.

Current Promotions

Is there a current promotion?

Worth It or a Scam?

If you have made it this far, it is probably clear that we think that Betterment is definitely worth checking out.

The company which was founded by Jon Stein and several others in 2008 (launched in 2010) can definetely be trusted.

The New York City-based company is a registered investment advisor (RIA) and a broker-dealer.

Furthermore, Betterment is a member of the Financial Industry Regulatory Authority (FINRA)

Summary

Once you have decided on a portfolio there is really no need to baby-sit your investment as your portfolio will be optimized automatically.

The interface is intuitive and transparent, optimization includes constant rebalancing and tax-loss harvesting.

Their fees are low and there is no minimum investment amount.

Who is it best for?

Betterment is best for passive investors. If you are looking to invest your money with a hands-off approach, Betterment is the way to go.

The platfom is great for beginners and advanced investors alike.

Who should look for a different service?

The DIY-investment crowd who is less reliant on personal advice will be better off with a different service like M1 Finance for example. Betterment only allows ETF investing which, for those with more complex investing needs, may be too narrow.

Robo Chooser

Use the following Quiz and find out which robo advisor is best for you.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team

Most robo-advisors help with your individual retirement accounts (IRA, Roth IRA, and SEP IRA) but not your 401K.

Blooom works with both your individual and employer-sponsored retirement accounts, but not in the traditional manner that most robo-advisors work.

Blooom is affordable, legitimate, and a great way to stay on top of your retirement funds.

Are you ready to learn more about this unique robo-advisor? Keep reading.

What is Blooom?

Have you ever wondered if your 401K could perform better? Maybe you don’t even know how it performs or what you invest in. Blooom ends those worries and questions by offering 401K and IRA advisory services.

Blooom also oversees your individual retirement accounts. The algorithm makes sure your accounts are on track to meet your retirement goals, whether you’re retiring in 5 years or 30 years. Blooom works with 401K accounts at any employer (as long as you have online access) or IRA providers with Fidelity, Charles Schwab, or Vanguard only.

How does it work?

Account Opening

Blooom only requires access to your online IRA or 401K account. It analyzes your account and tells you where you should make changes. Initially, the service is free, but if you want ongoing management services, there’s a fee, which we discuss in detail below.

There’s no minimum account balance or contributions you must make. You don’t transfer your fund to Blooom – it stays where it is and Blooom implements the changes as it recommends (depending on the program you choose) if you opt for their paid services.

The initial evaluation is free for anyone. You can do what you want with the information. If you don’t want to commit to the service, you can implement the suggested fund allocation yourself. If you want Blooom to manage it for you, sign up for a full account and enjoy hands-off investing.

Interface

Blooom’s interface is easy to use. After you answer simple questions about your risk tolerance, age, and retirement goals, Blooom recommends an asset allocation based on diversification, fees, and allocation.

Blooom evaluates your account every 95 days to make sure you’re still on target. If you ‘drift’ away from the target, they’ll reallocate your funds to get you back on track.

Trading options

Blooom is restricted to the funds in your IRA or 401K lineup. They diversify your assets between stocks and bonds, based on the risk tolerance and retirement goals you stated and what your plan offers.

Costs

Blooom works on a fixed-rate program, which works well for some people. If you’re trying to decide if it’s a good fit for you, calculate the fee as a percentage of your assets under management. Most robo-advisors charge anywhere between 0.25% and 0.50% of assets under management.

Compare your Blooom fee to that amount to get a good idea. For example, if you have $10,000 invested and you choose the Essentials plan, it would cost you 0.95% of assets under management. But, if you had $100,000 invested, it would only be 0.095% of assets under management.

Blooom offers the following plans:

Essentials $95/year – Get a personalized portfolio after evaluating your current investments and available plan funds and minimizing hidden investment fees. This plan doesn’t include automatic optimization.

Standard $120/year – Get a personalized portfolio, like in the Essentials plan but with automated optimization and access to an advisor (2 – 3 day turnaround time on answers).

Unlimited $250/year – Provides everything in the Standard plan, plus priority access to a financial advisor.

Additional features

Customer service – Blooom offers email and live chat during regular business hours, Monday – Friday 9 AM to 4 PM CT

Financial advisors – Blooom has human financial advisors on staff. If you sign up for the Standard or Unlimited plan, you may contact them but only via chat or email. Human advisors oversee all accounts, ensuring optimal portfolios periodically as well.

Automatic optimization – Blooom optimizes your account at least every 95 days. They base it on the amount of ‘drift’ your account makes. This refers to the amount the account moves away from the allocation originally set. If they don’t re-optimize your account within 95 days it means you’re still within means of reaching your goals.

Video

Blooom Pros and Cons

PROs

No minimum investment - Blooom doesn’t require a specific balance or deposit amount to evaluate and manage your account. Anyone with a qualified retirement plan may use the service.

CONs

Only certain IRAs qualify – Blooom works with any 401K custodian, but if you have an IRA, it must be with Fidelity, Vanguard, or Charles Schwab to qualify.

Acts as a fiduciary – Blooom must work to your benefit, not their own. In other words, they must recommend investments that align with your goals and overall financial needs, not their commission.

Blooom doesn’t ask you before making changes – When you sign up with Blooom, you agree to discretionary management, which gives Blooom the approval to make any and all trades that work in your fiduciary benefit. While the changes are usually ‘good’ it can be hard to give up that control.

No phone support – If you prefer talking to representatives on the phone, you won’t get it with Blooom.

Everyone gets a free analysis – If you aren’t sure if Blooom is for you, take advantage of their free analysis. There are no strings attached. See what they have to say and if you agree. If you don’t like it, you don’t have to sign up.

-

Anyone can use it – You don’t need your employer’s approval to sign up for Blooom. It’s a self-selected service that anyone can use.

-

PROs

No minimum investment - Blooom doesn’t require a specific balance or deposit amount to evaluate and manage your account. Anyone with a qualified retirement plan may use the service.

Acts as a fiduciary – Blooom must work to your benefit, not their own. In other words, they must recommend investments that align with your goals and overall financial needs, not their commission.

Everyone gets a free analysis – If you aren’t sure if Blooom is for you, take advantage of their free analysis. There are no strings attached. See what they have to say and if you agree. If you don’t like it, you don’t have to sign up.

Anyone can use it – You don’t need your employer’s approval to sign up for Blooom. It’s a self-selected service that anyone can use.

CONs

Only certain IRAs qualify – Blooom works with any 401K custodian, but if you have an IRA, it must be with Fidelity, Vanguard, or Charles Schwab to qualify.

Blooom doesn’t ask you before making changes – When you sign up with Blooom, you agree to discretionary management, which gives Blooom the approval to make any and all trades that work in your fiduciary benefit. While the changes are usually ‘good’ it can be hard to give up that control.

No phone support – If you prefer talking to representatives on the phone, you won’t get it with Blooom.

-

-

FAQ

Is Blooom safe?

Blooom protects your security with bank-level security and 256-bit encryption. Since they don’t take possession of your investments or handle your money, they don’t have SIPC coverage, but your plan should offer that.

Blooom protects any information they obtain from you, though, keeping it private and even alerting you of any withdrawals.

Are there other fees besides the management fee?

Blooom only charges its annual management fee, based on the plan you choose. However, there are always other fees, including commissions, transaction fees, and plan fees. Blooom does its best to minimize your costs, which is one of the main reasons to use the service, to decrease the fees eating at your retirement funds.

Does Blooom manage more than 401K and IRAs?

Yes, Blooom manages any type of retirement fund including traditional and Roth IRAs, 401K, 403(b), 457s, and 401(a) accounts. They manage all employer-sponsored accounts and IRAs with Fidelity, Charles Schwab, or Vanguard.

How many times a year does Blooom rebalance my portfolio?

On average, Blooom rebalances portfolios every 95 days, but not always. If your account has a lot of drift, they may rebalance it before 95 days. If it doesn’t drift at all (you’re on plan) and they don’t readjust it at all. They adjust the average account 3 – 4 times a year.

Do I need to move my 401K or IRA for Blooom to manage it?

No, your account stays put. Blooom manages it as a fiduciary. Blooom works with any 401K plan as long as you have online access. They only work with IRAs from Charles Schwab, Fidelity, and Vanguard, though.

How will I know if Blooom made changes to my account?

If Blooom optimizes your account, they will send you a notice that they made changes. Expect the optimizations to occur every 95 days unless your account drifts significantly and they feel it’s necessary to re-optimize it sooner.

Does Blooom support family accounts?

If you and your spouse or other family members each have retirement accounts, you must sign up for individual Blooom accounts. Each membership only manages one family member as each person has different needs based on their age, goals, and risk tolerance.

How does Blooom make money?

Blooom offers a free analysis, but if you want Blooom to do the work for you – implementing the ideal portfolio, there are fees as I discussed above. Most investors sign up for a plan, letting Blooom manage their retirement funds.

Alternatives

Blooom vs Personal Capital

Personal Capital is the closest alternative to Blooom, but they don’t actively manage your funds. They’ll evaluate your 401K and suggest a specific portfolio, but must do the work.

If you want a more hands-on approach to managing your 401K or IRA, Personal Capital offers the best of both worlds.

Bloom vs Wealthfront

Wealthfront doesn’t manage your 401K or provide any advice regarding your 401K. They do offer 401K rollover services, though, if you leave your job and need a place for your retirement funds. Wealthfront has a $500 minimum opening balance requirement and charges 0.25% of assets under management each year.

It’s great for investors with a 401K that don’t know where to invest it without incurring tax penalties.

Blooom vs Betterment

Betterment doesn’t have a minimum balance required. You can open an IRA or taxable brokerage account, but they don’t manage your 401K. However, Betterment offers 401K rollover services either into an IRA or a Betterment 401K if your new employer offers one. Betterment charges 0.25% of assets under management.

They also offer tax-loss harvesting, making it a great option for borrowers with a large amount invested and high tax liabilities.

Blooom vs Target Date Fund

Blooom often gets compared to Target Date Funds, as they are the most common option for 401Ks. It makes sense – you enter your retirement date and choose the fund that allocates your investments to meet your retirement goal.

Blooom, however, allocates your money differently, and re-optimizes it ever 95 days to make sure you’re on target. Target Date Funds are often too conservative and have higher fees. If you’d prefer a customized plan that suits your retirement needs including your targeted retirement date, consider Blooom instead.

Blooom vs Financial Engines

Financial Engines is an advisory service for retirement plans, including 401Ks. They work with larger companies, such as Delta, Ford, Kraft Foods, and Microsoft, to name a few.

Financial Engines either manages your plan for you or evaluates your plan and tells you how to manage it. Financial Engines is only available if your employer offers it as a service.

Current Promotions

There are currently no promotions.

Worth It or a Scam?

Blooom is worth it for many investors, especially those with a large 401K balance. While its fees can eat into the accounts of investors with less money invested, it does help you avoid unnecessary fees. If you prefer a hands-off approach to investing, but want to maximize your retirement earnings, Blooom is worth it for most people.

Bottom Line

Blooom offers a unique service that most robo-advisors don’t offer. If you are confused about your 401K offerings or you worry that you’re paying high fees that take away from your retirement funds, consider letting Blooom get you back on track.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team

When you have done some research on investing, the name M1 Finance will inevitably become part of your vocabulary.

The fast-rising online investing platform is among the most popular, especially among young investors.

M1 Finance is a robo advisor but it couldn’t be more different than the classic robos like Schwab, Vanguard or Betterment.

Check out my in-depth review to find out why!

What is M1 Finance?

M1 Finance is basically a mix between true robo advisor and online brokerage (You can not only invest in ETFs but also in individual stocks).

It is a purely algorithm-based tool that doesn’t rely on any human advice.

The goal based investing approach is a great choice for beginners, and also for advanced investors as it comes with a variety of tools and options. The platform also allows for a lot of customization.

M1 is for people who are interested in investing. If you are looking for more of a hands-off robo advisor you are probably better off with one of the classics like Wealthfront or Betterment.

M1 Finance has amassed a huge number of investors since its establishment in 2015.

To see what the fuss is all about read on and find out everything you need to know in this in-depth review.

Note: Investing in a certain robo advisor will have a huge impact on your overall financial future.

That is why I recommend reading this review to the very end. You really need to know as much as possible about the different options in order to understand what is really important to you.

M1 Finance – How does it work?

Everything you need to know from opening an account to actively managing your investment portfolio.

1. Open An Account

Start by opening an M1 Finance account here.

Let’s look at the whole process:

1. Create a pie

2. Open your account

3. Fund your account

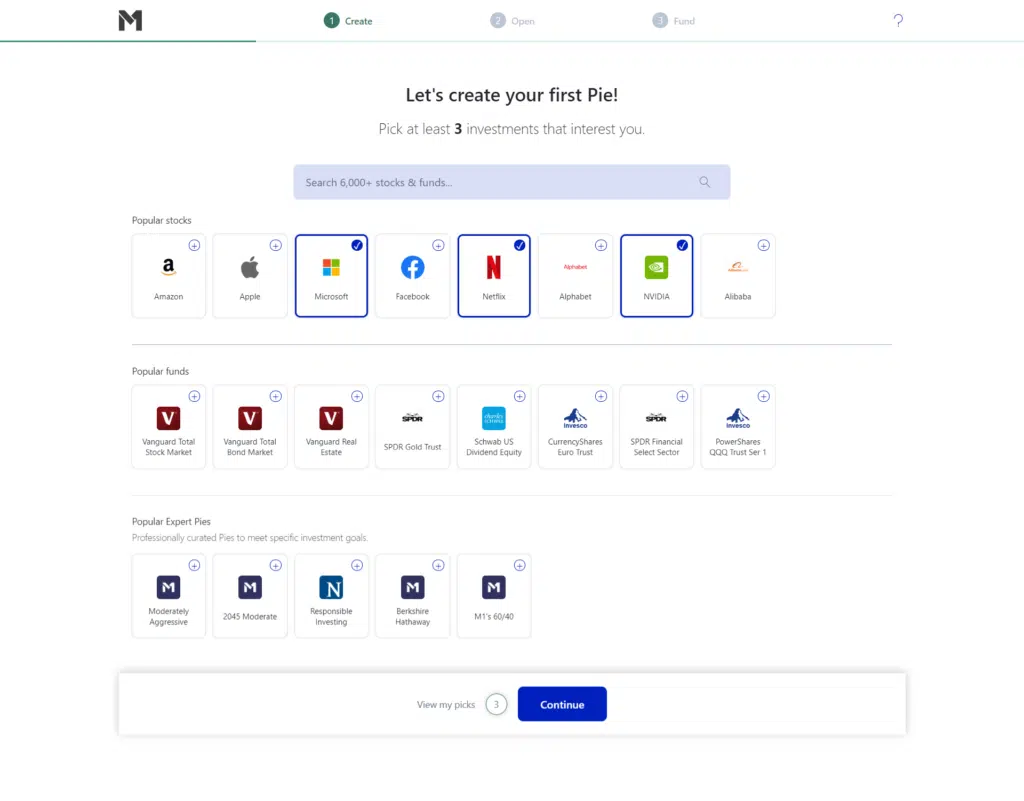

Signing up is easy, you enter your email and a desired password, then you will be forwarded to a page that let’s you create your first pie. (Contrary to most other robo advisors, there are no questions as far as risk assessment goes)

Now you can start and build your own pie or choose one made up of ETFs or individual stocks.

For starters you will be asked to pick at least three ETFs that you would like to invest in.

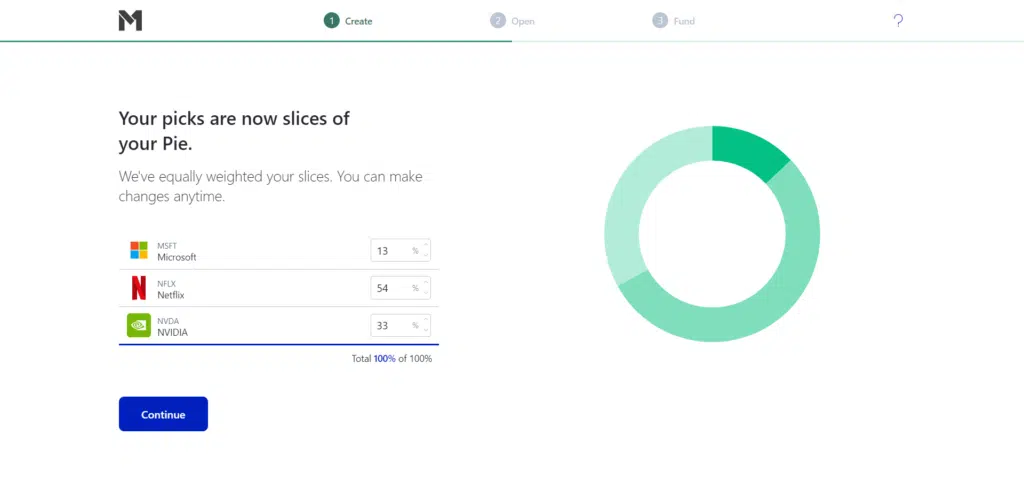

To keep things simple, in the example above I selected Microsoft, Netflix and Nvidia.

Your finished portfolio will probably (hopefully) look a lot different than this one but as a tutorial to show you how the site works it is just perfect. You can practice a little and chose different combination.

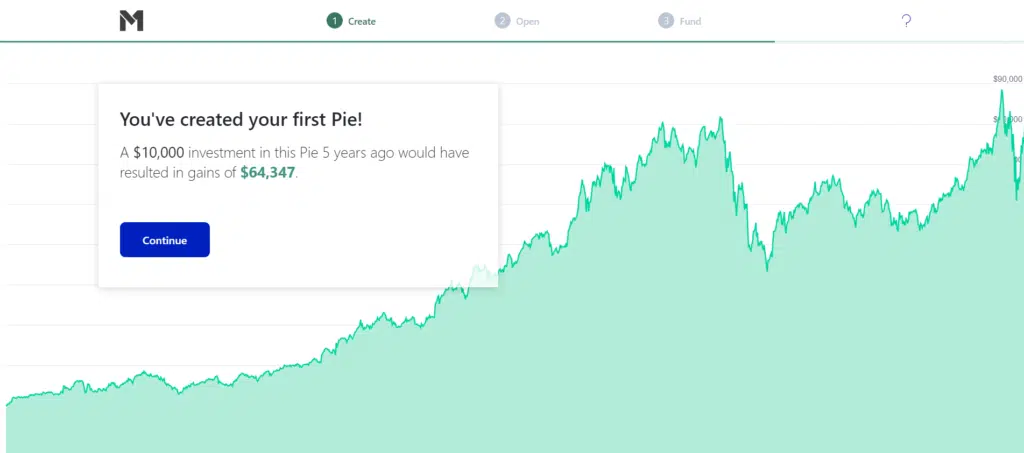

Although this serves as mostly marketing purposes, I found it quite interesting to see how my porfolio would have performed if I had invested in it 5 years ago.

The next step will be to enter your personal information and link a bank account. The following are elegible:

Traditional IRA

Roth IRA

Taxable Investment Accounts

SEP IRA

Trust Accounts

Rollover IRA

2. Deposit and withdrawal

Choose the funding option from within your account, there you can easily deposit your money. You can also set up automated deposits with a certain amount of money every month.

You can only do one withdrawal at a time. If you currently have a withdrawal request in process, you won’t be able to schedule another until the first one completes. This is important to know in case you want to spend your money elsewhere. (It can take 2-4 business days for funds to arrive in your bank account

3. Pies explained (Video)

The “pie” investment templates are pretty cool. You get to choose from many pre-built pies, or you can customize one of your own.

You may look at this as a gimmick, and yes you do have a point, however the pies make it easy to view the investment allocations at a single glance.

The portfolio management (pie management i guess) is best explained by a video. Credit goes to David Caruana, thanks for making this awesome tutorial.

Once you know your way around the pies there are a couple of things that are important to note:

The time all trades are made is 9AM CEST.

The moment your account reaches $10, your money will automatically be invested.

What can you invest in?

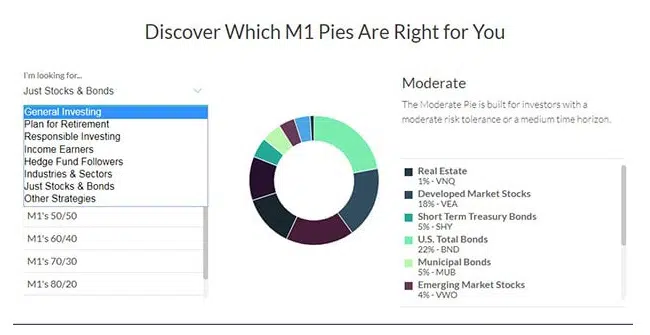

M1 Finance offers a ton of customization, depending on your goals you can select one of the following categories:

General Investing: Anything. Based on your level of risk tolerance.

Plan for Retirement: Set a retirement date and start to customize your portfolio accordingly.

Responsible Investing: Invest socially and environmentally friendly.

Income Earners: This category is designed to invest based on dividends and income returns.

Hedge Fund Followers: This is an approach where you are using the same strategies of successful investors.

Industries and Sectors: Currently not available

Just Stocks and Bonds: This is a diversified portfolio with a total world stock fund, and a bond fund.

Other Strategies

Costs or hidden fees?

M1 Finance does not have an annual fee and also doesn’t charge for trading. So of course you may wonder, where are the hidden fees?

You can create as many custom pies as you like without being charged for it. However there is something M1 charges for, and that’s the termination fees. So for example if you open a retirement account and later decide to close it, a $100 account termination fee is imposed (this may sound harsh but is actually standard at brokerage firms).

Moreover, M1 Plus comes with an annual fee of $100 for the first year and $125 per year after that. There is also an inactivity fee. This fee applies whenever the user stays offline for more than 180 days. ($20)

As mentioned earlier, M1 is not a hands-off platform, it is best suited for people who are actually interested in entering the world of investments.

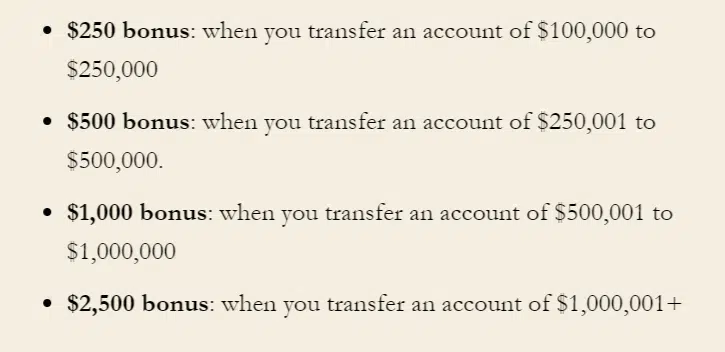

M1 Bonus offers

If you are willing to invest a big chunk of money, this is how M1 will reward you:

Support and user experience

They have a platform where you can find answers. Also phone support and email support. This is not to be confused with financial advice. M1 has no human financial advisors. Support is merely there to help you with technical issues.

The phone number is (312) 600-2883 and the

Support email is: support@m1finance.com.

Goal setting

As mentioned earlier M1 does have somewhat of a goal setting feature. If you are interested in socially responsible investing or investing for retirement for example, then there is an option to customize your portfolio towards that goal.

But if we are talking about actual financial planning then M1 is not the place to find it. M1 targets users who are already somewhat familiar with the investments and serves more as a DIY platform.

Pick short-term investment goals based on your current consumer habits. For instance, you might want to upgrade your old furniture, make a home improvement or gradually divert some income toward a vehicle down payment.

Choose long-term goals for investing with an eye on your ideal future. This is where you think about saving to fund a comfortable retirement, your children’s college fund, or buy a new home.

M1 Finance Pros and Cons

PROs

No account fees

CONs

No human (or digital) advisors

Option to borrow money against the value of your portfolio

Fairly new brokerage, accounts are protected up to $500,000 (SIPC)

Choose your own investments

You can only trade once or twice a day (M1 Plus members with a min. balance of $25,000 can trade during both windows while members with a balance of less than $25,000 can only trade once a day)

Option to invest in individual stocks & fractional shares

If you want to trade options you will need a different brokerage

Great, intuitive platform (lets you creat a very diversified portfolio)

-

Great for every experience level

-

Rebalancing is automated

-

The initial deposit of only $100 is a great incentive to just try it out and get your feet wet

-

PROs

No account fees

Option to borrow money against the value of your portfolio

Choose your own investments

Option to invest in individual stocks & fractional shares

Great, intuitive platform (lets you creat a very diversified portfolio)

Great for every experience level

Rebalancing is automated

The initial deposit of only $100 is a great incentive to just try it out and get your feet wet

CONs

No human (or digital) advisors

Fairly new brokerage, accounts are protected up to $500,000 (SIPC)

You can only trade once or twice a day (M1 Plus members with a min. balance of $25,000 can trade during both windows while members with a balance of less than $25,000 can only trade once a day)

If you want to trade options you will need a different brokerage

-

-

-

-

FAQ

What is M1 Spend?

M1 Spend is basically the name of M1s debit card. (free) It integrates with your investments and portfolio line of credit. You can use it to

transfer money instantly and set up direct deposits

pay back your loan on your schedule

invest automatically on a schedule

The ATM fees are only reimbursed once per month. So if you use ATMs often, this may not be the your best choice.

What is M1 Plus?

M1 Plus is the better version of M1 Spend. It carries an annual fee of $125. The benefits are

1.5% APY checking account

1% cash back on all debit purchases

Up to 4 ATM fees are reimbursed (per month)

You can get an extended afternoon trading window

0.25% discount on borrow rates when accessing their extended portfolio credit line, which brings us to the next question…

What is M1 Borrow?

M1 Borrow is a service that lets you access a flexible portfolio line of credit, the rate is actually lower than the average personal loan or mortgage.

Is M1 Finance legit?

Yes, M1 is registered as a broker with FINRA and are SIPC.

Can you open a Roth IRA retirement account with M1?

Yes, the M1 Finance Roth IRA is just as good as any Roth IRA being offered elsewhere.

Can you trade on M1?

Yes, there are 2 trading windows. Depending on your account you can either trade once or twice daily.

What happens if M1 Finance goes out of business?

Should M1 ever go out of business, your investments are protected up to $500,000. Obviously, SIPC does not protect you from losing money through investing.

Does M1 Finance pay dividends?

Yes. The moment your total amount of dividends reaches $10 the money is automatically reinvested into your portfolio.

Current Promotions

Is there a current promotion?

Best for DIY

Account Minimum

$100

Management Fee

0.00%

Portfolio

The user can create portfolios which consist of low-cost ETFs or individual stocks

Account Types

Individual and joint taxable accounts; traditional, Roth and rollover IRAs, trusts and even business accounts.

Rebalancing

Tax Loss Harvesting

Fractional Shares

Automatic Deposits

SRI

Human Advice

Best for

DIY Investors. If you are enthusiastic about getting your feet wet in the investing world, M1 Finance is the robo advisor of your choice

Summary

M1 Finance is the best choice for self-directed investors that want to pick from existing portfolios or customize their own.

Betterment gives you financial advice and has a high focus on customer service and goal planning. It is more of hands-off robo advisor.

M1 Finance definetely beats Betterment in the fees department. The portfolios you create allow more flexibility. Check out this article to read the whole comparison.

M1 Finance vs Robinhood

RobinHood has the benefit that it allows you to invest in crypto and options. What M1 Finance and Robinhood have in comon is that both offer fractional shares.

It could be argued that Robinhood is a more beginner friendly platform while M1 Finance offers features that are geared towards long term investments. The min. account balance with M1 is $100 while RobinHood has no min. account balance

M1 Finance vs Wealthfront

Of course M1 Finance beats every competitor as far as fees, Wealthfront for example has a (low) fee of 0.25%. The account minimum is $500 The benefit Weathfront has over M1 is its advanced planning tools to help provide a complete picture of your financial health and track your goals. Check out our complete comparison here.

M1 Finance vs Vanguard

Vanguard is great for people who have a lot of money to invest. If you are at a point where you need a personal advisor, Vanguard is probably the way to go. Read or in-depth review and learn all the differences between these two platforms.

M1 Finance vs Webull

Webull is a platform for day traders. So there is really not all that much to compare. Of course trading with M1 is possible however trades do not execute immediately, only during the trading windows. Moreover, you can only place market orders which is another disadvantage.

What these two platforms have in common are the fact that they are extremely low-cost and easy to use. Check out all the advantages and disadvanages both platforms have to offer in this review.

Worth It or a Scam?

M1 Finance is definetely not a scam. We are talking about a SEC registered broker-dealer and a member of FINRA and SIPC. There are I guess what you could refer to as “hidden fees” like the fact that they charge a $20 fee on the sale on shares in a mutual fund however in my opinion the extremely low fees make up for that.

Security

Security should be of very little concern when talking about M1 Finance. The website uses 4096-bit encryption for data transfers.

Your investments are covered with insurance of up $500,000. (SIPC)

Of course it also allows you to set up two-factor authentication, fingerprint verification and face recognition. (mobile only)

Summary

M1 Finance is best for self-directed investors. If you are into DIY investing, regardless of experience level, M1 is the way to go.

The focus is overall growth of assets. Simply put, unlike other advisors, M1 doesn’t care why you are investing, but it helps you do it better and more efficiently.

On top of that, it can be ideal for clients who want to place socially conscious investments.

The way M1 Finance sets itself apart from other tools and platforms like Vanguard or Wealthfront, are the extremely low fees and ease of access.

Robo Chooser

Use the following Quiz and find out which robo advisor is best for you.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team

You have just retired or are planning to retire soon.

Your focus now is on cash-flow, not so much on earnings. You just need to make sure you have enough to get you through the next 30 years without a paycheck coming in.

The good news is, if you invest with the right robo advisor, you don’t have to bother with any complicated investment decisions when you’re retired.

Best Robo Advisors for Retirees – My Top 3 Picks

Robo-advisors aren’t just for millennials – retirees benefit too. In fact, it’s almost more important for retirees to take advantage of this great investing service.

Which robo-advisor is right for you? Check out my favorites below.

Best

Low Cost

Account Minimum

$100,000

$5,000

$500

Management fee

The management fee for accounts between $1,000,0000-$3,000,000 is 0.89%. Once the account reaches $10,000,000 the fee will drop to 0.49%.

0.50%

0.25%

Portfolio

Customized for each client

14 different ETFs

ETFs from 11 different asset classes

Rebalancing

Tax Loss Harvesting

Smart Beta

Socially Responsible Investing

Human Advice

401(k) Assistance

Summary

Personal Capital has great financial management tools. The fees are on the higher end however this service is perfect for high net worth investing with access to human financial planners.

FutureAdvisor is the middle ground so to speak. The fees are slightly above average but they do offer a great service with free tools and human advice.

Wealthfront uses a low-cost, hands-off investing approach. The service is completely software-based so if you are looking for a dedicated human advisor it would be better to look elsewhere.

The management fee for accounts between $1,000,0000-$3,000,000 is 0.89%. Once the account reaches $10,000,000 the fee will drop to 0.49%.

Portfolio

Customized for each client

Rebalancing

Tax Loss Harvesting

Smart Beta

Socially Responsible Investing

Human Advice

401(k) Assistance

Summary

Personal Capital has great financial management tools. The fees are on the higher end however this service is perfect for high net worth investing with access to human financial planners.

FutureAdvisor is the middle ground so to speak. The fees are slightly above average but they do offer a great service with free tools and human advice.

Wealthfront uses a low-cost, hands-off investing approach. The service is completely software-based so if you are looking for a dedicated human advisor it would be better to look elsewhere.

Personal Capital takes the cake for best robo-advisor for retirees. It offers the perfect combination of digital advisor and human advisor, not to mention its holistic approach to investing that is personalized, rather than generalized.

Features

Personal financial analysis – Personal Capital looks at more than your investments. They help you look at the big picture. Are you worried about overspending during retirement? Personal Capital will help you see where you overspend, what you can change, and of course, how you can structure your investments based on your risk tolerance.

Access to personal financial advisors – This is something that sets Personal Capital apart from all others. Everyone has access to a team of financial advisors for human advice. If you have more than $200,000 invested get two dedicated financial advisors.

You need a minimum of $100,000 invested – Retirees should have a lot more than $100,000, so this shouldn’t be hard to achieve

Access to many account types – You can open retirement accounts, non-retirement accounts, trusts, and even a cash account

PROs

You get a full view of ALL of your finances from your checking account to your retirement accounts and everything in between. Everything is located in one dashboard.

CONs

You must adhere to Personal Capital’s asset allocation. It’s not customizable, which may not work for investors that like to tweak their portfolios.

Personal Capital offers a You Index which is a personalized look at your holdings except for your cash, money market funds, and bonds. It’s a good indicator of how your investments are performing over time.

Some people may think the wealth management fees are excessive.

You pay one fee only so it’s easy to determine your costs rather than paying individual commissions and hidden fees.

You need at least $100,000 to use the wealth management services.

Tax Loss Harvesting

Your personal advisor may not be the same person each time ... unless you have at least $200,000 invested

Get up-to-date spending suggestions or investment changes whenever you make changes to your Social Security income or spending, or other changes.

-

Low ETF expense ratios

-

Great for investors that want a hybrid between human advisors and automated robo-advisors

-

PROs

You get a full view of ALL of your finances from your checking account to your retirement accounts and everything in between. Everything is located in one dashboard.

Personal Capital offers a You Index which is a personalized look at your holdings except for your cash, money market funds, and bonds. It’s a good indicator of how your investments are performing over time.

You pay one fee only so it’s easy to determine your costs rather than paying individual commissions and hidden fees.

Tax Loss Harvesting

Get up-to-date spending suggestions or investment changes whenever you make changes to your Social Security income or spending, or other changes.

Low ETF expense ratios

Great for investors that want a hybrid between human advisors and automated robo-advisors

CONs

You must adhere to Personal Capital’s asset allocation. It’s not customizable, which may not work for investors that like to tweak their portfolios.

Some people may think the wealth management fees are excessive.

You need at least $100,000 to use the wealth management services.

Your personal advisor may not be the same person each time ... unless you have at least $200,000 invested

-

-

-

2. FutureAdvisor

FutureAdvisor offers free retirement planning and account management, which is great for retirees trying to maximize their funds during retirement.

FutureAdvisor advises on TD Ameritrade and Fidelity accounts, so if you don’t have a brokerage account there, you must open one.

Features

ETF expense ratios from 0.14% to 0.18% – These low-cost ETFs help retirees make the most of their investments. You want to keep your portfolio conservative, but still growing and with low-cost ETFs, that’s possible.

Manages all accounts – FutureAdvisor oversees taxable and retirement accounts, helping you figure out the best way to maximize your income while you aren’t working and need to ensure you have enough funds for the rest of your life.

Tax-loss harvesting – It’s even more important to keep your tax liabilities low when you’re retired, as you need every penny you can keep during this time.

Human advisors – Get access to human advisors during regular business hours, which can be great to help maximize your savings and spending during retirement

PROs

Get a second opinion on your investments – Who doesn’t love a second opinion on their chosen investments? Consult with a personal advisor at FutureAdvisor to make sure you’re on the right track.

CONs

High fees - Be careful with management fees as they eat away at your earnings and right now, you need every penny you can get.

Free financial planning tools - You can get an analysis of your portfolio before you transfer it over if you are unsure of FutureAdvisors can help you make a difference

You must have a TD Ameritrade or Fidelity account - If you don’t have an account at one of the two brokers already, you must transfer your assets there if you want FutureAdvisors to manage them.

Automatic Rebalancing - If your portfolio gets knocked sideways, you’ll get an alert to rebalance it, giving you a chance to stop disaster before it occurs.

No socially responsible investing

Choose from 12 asset classes - Diversify your investments to minimize your risk during this crucial time in your life with the asset classes.

No fractional shares

PROs

Get a second opinion on your investments – Who doesn’t love a second opinion on their chosen investments? Consult with a personal advisor at FutureAdvisor to make sure you’re on the right track.

Free financial planning tools - You can get an analysis of your portfolio before you transfer it over if you are unsure of FutureAdvisors can help you make a difference

Automatic Rebalancing - If your portfolio gets knocked sideways, you’ll get an alert to rebalance it, giving you a chance to stop disaster before it occurs.

Choose from 12 asset classes - Diversify your investments to minimize your risk during this crucial time in your life with the asset classes.

CONs

High fees - Be careful with management fees as they eat away at your earnings and right now, you need every penny you can get.

You must have a TD Ameritrade or Fidelity account - If you don’t have an account at one of the two brokers already, you must transfer your assets there if you want FutureAdvisors to manage them.

No socially responsible investing

No fractional shares

3. Wealthfront

New and experienced investors love Wealthfront’s many benefits and low management fee.

You only need $500 to get started and they charge just 0.25% of assets under management for this automated robo-advisor service.

Features

ETF management fees of just 0.08% – Keeping your fees to a minimum is important right now when you’re not earning money and rely on your investments.

Manage a variety of accounts – Whether you have taxable or retirement accounts, Wealthfront manages them all, helping you to maximize your income.

Daily tax-loss harvesting – Why pay more taxes than necessary, especially during retirement? Wealthfront automatically looks for tax-loss harvesting opportunities to save you money.

Automatic rebalancing – If your portfolio starts going the wrong direction, Wealthfront automatically rebalances it for you.

PROs

Low ETF expense ratios

CONs

Wealthfront’s advanced features are reserved for investors with at least $100,000

A large number of investment options

You can’t buy fractional shares

Low annual management fees

You can only get customer service via phone, no online chat

Free financial planning tools that even non-Wealthfront clients can use

You need at least $500 to get started

Earn interest on your cash account

-

Regular tax-loss harvesting

-

Automatic rebalancing

-

Help setting financial goals

-

Line of credit available for large investors

-

PROs

Low ETF expense ratios

A large number of investment options

Low annual management fees

Free financial planning tools that even non-Wealthfront clients can use

Earn interest on your cash account

Regular tax-loss harvesting

Automatic rebalancing

Help setting financial goals

Line of credit available for large investors

CONs

Wealthfront’s advanced features are reserved for investors with at least $100,000

You can’t buy fractional shares

You can only get customer service via phone, no online chat

You need at least $500 to get started

-

-

-

-

-

Alternatives

Vanguard

If you have $50,000 or more in an investment account, Vanguard is a great option. This hybrid robo-advisor offers the best of both worlds between human advice and automated investing.

A player in the industry already, Vanguard has quite a following, but its robo-advisor is somewhat new and suitable for many investors.

Features

Access to a team of financial advisors – Get help with Social Security optimization, best use of your retirement funds, or investment advice.

Customizable portfolio construction – This isn’t a one-size-fits-all approach. Vanguard customizes your portfolio based on the advisor’s thoughts and the information you provide.

Open any type of account – Vanguard offers taxable, retirement, and trust accounts.

Access to customer service reps – You can talk to a rep Monday – Friday from 8 AM to 8 PM.

PROs

Vanguard advisors don’t make a commission – All Vanguard advisors have a fiduciary obligation to do what’s in your best interest. They don’t make a commission off your investments, so you don’t have to worry about feeling pushed into specific investments.

CONs

You need at least $50,000 – This can be out of reach for beginning investors. Most robo-advisors have much lower investment requirements if any so this puts Vanguard in a league of its own.

Low costs – While 0.3% of assets under management sounds like a lot, if you compare it to a traditional full-service broker, you’ll see that you’re saving thousands of dollars. Of course, there are nuances that go along with it, but the savings is worth its weight in gold.

No tax loss harvesting – Large investors almost always want to take advantage of tax loss harvesting as it lowers your tax liability. Vanguard doesn’t offer this, but they do try to make your trades/settlements as tax efficient as they can without using the words tax loss harvesting.

You can track your progress 24/7 – Any time you want to know how your portfolio’s doing or how close you are to reaching your goal, you just have to log into your dashboard. You can talk to your advisors at any point too, so if you feel nervous or think your portfolio is too far off course, call your advisor.

Not the friendliest website – Typically, robo-advisor websites are chock full of tools and research, but not Vanguard. They rely mostly on your conversations with a financial advisor, rather than providing you with education, research, or even tools on their website.

Vanguard funds are among the lowest costing investments – In addition to its low assets under management fees, Vanguard ETFs are among the lowest cost investments on the market. (That is also why other robo advisors invest in their ETFs as well)

-

PROs

Vanguard advisors don’t make a commission – All Vanguard advisors have a fiduciary obligation to do what’s in your best interest. They don’t make a commission off your investments, so you don’t have to worry about feeling pushed into specific investments.

Low costs – While 0.3% of assets under management sounds like a lot, if you compare it to a traditional full-service broker, you’ll see that you’re saving thousands of dollars. Of course, there are nuances that go along with it, but the savings is worth its weight in gold.

You can track your progress 24/7 – Any time you want to know how your portfolio’s doing or how close you are to reaching your goal, you just have to log into your dashboard. You can talk to your advisors at any point too, so if you feel nervous or think your portfolio is too far off course, call your advisor.

Vanguard funds are among the lowest costing investments – In addition to its low assets under management fees, Vanguard ETFs are among the lowest cost investments on the market. (That is also why other robo advisors invest in their ETFs as well)

CONs

You need at least $50,000 – This can be out of reach for beginning investors. Most robo-advisors have much lower investment requirements if any so this puts Vanguard in a league of its own.

No tax loss harvesting – Large investors almost always want to take advantage of tax loss harvesting as it lowers your tax liability. Vanguard doesn’t offer this, but they do try to make your trades/settlements as tax efficient as they can without using the words tax loss harvesting.

Not the friendliest website – Typically, robo-advisor websites are chock full of tools and research, but not Vanguard. They rely mostly on your conversations with a financial advisor, rather than providing you with education, research, or even tools on their website.

-

Acorns

It started as the ‘spare change’ investor, but today, Acorns offers many features. It’s a robo-advisor/automated saving tool that retirees can use to their advantage.

Whether you’re still working on your nest egg or you have a nice nest egg built and just want a simple tool to keep it strong, Acorns is a great tool.

Features

Round up your purchases – It’s never too late to round up your purchases to keep investing. During retirement, you still need to grow your earnings, so why not automate it?

Low ETF expense ratios – It costs just 0.03% – 0.18% for ETF expense ratios, which saves you money on expenses.

7 ETFs to choose from – While it’s not a lot, it keeps things simple and Acorns offers five portfolio options

Taxable and retirement accounts – You can open a taxable account and an IRA or Roth IRA

PROs

Everything’s automatic – If you don’t like thinking about depositing funds or making investments, let Acorns do it all for you from the savings to the investments.

CONs

Transfer fees – It costs $50 per ETF to have them transferred to another broker.

Connect as many cards as you wish – Acorns sweeps the spare change from every purchase on your cards into your investment account and then invests the money once you accumulate enough.

High monthly fees – You pay a monthly fee of $1 - $3 for Acorns. If you have $5,000 invested, that’s a 0.24% fee and you don’t get as many benefits as you would at say Wealthfront.

Small balance requirements – You only need $5 to start investing. While you obviously want more, it’s easy to get started and stay motivated.

-

Great for new investors – If you’re trying out something new, Acorns is a great place to try it. They offer plenty of educational opportunities and guidance.

-

-

-

-

-

PROs

Everything’s automatic – If you don’t like thinking about depositing funds or making investments, let Acorns do it all for you from the savings to the investments.

Connect as many cards as you wish – Acorns sweeps the spare change from every purchase on your cards into your investment account and then invests the money once you accumulate enough.

Small balance requirements – You only need $5 to start investing. While you obviously want more, it’s easy to get started and stay motivated.

Great for new investors – If you’re trying out something new, Acorns is a great place to try it. They offer plenty of educational opportunities and guidance.

-

-

CONs

Transfer fees – It costs $50 per ETF to have them transferred to another broker.

High monthly fees – You pay a monthly fee of $1 - $3 for Acorns. If you have $5,000 invested, that’s a 0.24% fee and you don’t get as many benefits as you would at say Wealthfront.

-

-

-

-

Betterment

Betterment offers two services, Betterment Digital and Betterment Premium. The Digital program is for those with less than $100,000 invested, and the premium is for investors with more than $100,000 invested.

The fee is higher on the premium account, but you get more benefits.

12 asset classes – Choose from a large number of asset classes to help diversify your risk and reach your goals.

Offers many options – From socially responsible investing to smart beta investing, Betterment offers all of it, giving you options.

Open any type of account – Retirement accounts, taxable accounts, trusts, and cash accounts are all acceptable.

PROs

Perfect for easy, hands-off investing – Once you have set your goals you can lean back and let Betterment do the rest.

CONs

Difficult to cancel the account – Betterment makes it paperwork heavy to leave them.

Rebalancing and Daily tax-loss harvesting – Minimize your tax liabilities with daily tax-loss harvesting, selling off your losses to offset your gains

Encourages you to invest your emergency fund – Most financial experts recommend keeping your emergency fund liquid, but Betterment recommends a specific portfolio that is on the aggressive side and could put your emergency fund at risk.

Offers a variety of tools – Betterment helps you plan your financial future by making smart financial decisions with your investments and regular accounts too.

-

No minimum deposit – You don’t need any money to open an account, but even better is the low $100,000 minimum for Betterment Premium which offers access to professional financial advisors.

-

Low management fees – Betterment charges just 0.25% for less than $100,000 and 0.40% for over $100,000

-

PROs

Perfect for easy, hands-off investing – Once you have set your goals you can lean back and let Betterment do the rest.

Rebalancing and Daily tax-loss harvesting – Minimize your tax liabilities with daily tax-loss harvesting, selling off your losses to offset your gains

Offers a variety of tools – Betterment helps you plan your financial future by making smart financial decisions with your investments and regular accounts too.

No minimum deposit – You don’t need any money to open an account, but even better is the low $100,000 minimum for Betterment Premium which offers access to professional financial advisors.

Low management fees – Betterment charges just 0.25% for less than $100,000 and 0.40% for over $100,000

CONs

Difficult to cancel the account – Betterment makes it paperwork heavy to leave them.

Encourages you to invest your emergency fund – Most financial experts recommend keeping your emergency fund liquid, but Betterment recommends a specific portfolio that is on the aggressive side and could put your emergency fund at risk.

They look not only at investments but at financial planning too, as that’s an important aspect for retirees.

Features

Account sequencing – Prioritizes which accounts you should spend from while maintaining your investments in others to keep your earnings growing during this crucial time

Personalized budgeting recommendations – During this ‘new’ time in your life, you have to revamp your budget and United Income helps you do it

Plan your legacy – If you plan to leave behind a legacy, United Income helps you plan accordingly

Social Security advice – Learn how to maximize your benefit and make the most of the funds with the Social Security income advice that comes with every account.

PROs

Uses a smart beta approach – United Income tries to beat the market, not match it, for greater growth and earnings.

CONs

The sign-up process is complicated – You must call United Income to sign up, you can’t sign up online.

Diversification across 10 asset classes – United Income focuses on diversifying funds to keep your risk low and your earnings high

High fees – The management fee is 0.50% of assets under management, which is higher than most.

Offers tax-loss harvesting – All accounts are eligible, not just those with high balances.

-

Offers a holistic approach to finances – United Income looks at more than your investments; they help you figure out the big financial picture during retirement.

-

PROs

Uses a smart beta approach – United Income tries to beat the market, not match it, for greater growth and earnings.

Diversification across 10 asset classes – United Income focuses on diversifying funds to keep your risk low and your earnings high

Offers tax-loss harvesting – All accounts are eligible, not just those with high balances.

Offers a holistic approach to finances – United Income looks at more than your investments; they help you figure out the big financial picture during retirement.

CONs

The sign-up process is complicated – You must call United Income to sign up, you can’t sign up online.

High fees – The management fee is 0.50% of assets under management, which is higher than most.

-

-

[Bonus] SigFig

Best if you don’t want to move your funds to a different platform

If you don’t want to move your investments, but want the advice of a robo-advisor, check out SigFig. It works only with third-party brokerage platforms, namely Charles Schwab and Fidelity. The idea is to maximize your portfolio while leaving it where it is to avoid unnecessary fees.

You can choose the free Portfolio Tracker that tracks all of your investments in one place or the Asset Management Plan that balances and diversifies your investments, to increase your earnings. This service is free up to $10,000 invested and then 0.25% per year beyond $10,000 in investments.

SigFig gives advice on how to maximize your portfolio for the greatest results during retirement.

Do you really need a robo advisor for your retirement?

If you want advice to maximize your earnings and decrease your costs, don’t give up on robo-advisors just because you’re retired. Sure, they seem like they’re made just for millennials with the new technology and all the bells and whistles, but there are plenty of benefits for retirees too.

Honestly, where else can you get professional-grade investment advice for a fraction of what human advisors cost? Why spend an arm and a leg on a human advisor when you could manage the investments yourself with the help of a robo-advisor?

Thanks to the low overhead and automated processes, you can pay minimal fees, and yet have professional advice on how to reach your retirement goals. It’s no secret that life really changes once you retire and I’m talking financially. Rather than getting slapped in the face with the new money issues, have a robo-advisor on your side, helping you make the most of this time you’ve worked so hard to have feel financially free.

How Robo Advisors Manage a Retiree’s Portfolio

As you hit retirement, your portfolios need to change. No longer are you relying on the aggressiveness of a stock portfolio. It’s no longer about growth, but about keeping what you earned. If you stay in a heavy stock portfolio, you risk a lot – you could even risk it all. Does that make sense?

Robo-advisors change your portfolio to a more conservative, bond-heavy portfolio.

Just please make sure your risk tolerance reflects the fact that you’re retired, and the robo-advisor does the rest for you.

The difference in portfolios retirees vs non-retirees

As I said above, it’s about being conservative when you’re a retiree and robo-advisors understand that. You’ll move from a stock portfolio to a mostly bond portfolio. Don’t worry, you’ll still have earnings, they just won’t be as large. But the better news is that you won’t have losses. When you focus mostly on bonds, you get an almost guaranteed return.

Because your focus is on cash flow and not growth, you’ll focus on not losing money in your portfolio. Hopefully, by this point, you’ve accumulated enough earnings that you can live off of it and the minimal growth it will make in a more conservative portfolio.

Pros and Cons of a robo-advisor for retirees

Pros

You get a hands-off approach to investing

The portfolio automatically adjusts for you based on your new risk tolerance

You take advantage of tax-loss harvesting techniques

The fees are low compared to a human advisor

You don’t need a specific balance for most robo-advisors

You get tailored advice, sometimes even from a human advisor

Cons

You can’t get involved in the investments if you want to (some people prefer to)

You pay a percentage of your assets under management

You go from an aggressive portfolio to a conservative portfolio whether you want to or not

FAQ

Are robo-advisors good for retirees?

Robo-advisors are experts at assessing risk and telling how much you can risk, spend, and need to earn to reach your goals. While it seems like more of a feature for those approaching retirement, it’s also great for retirees.

How should you choose a robo-advisor?

Choose the robo-advisor that offers the services you need and the prices you can afford. Don’t focus on price alone, but also on the features. Does the robo-advisor offer tax-loss harvesting? What about automatic rebalancing or access to a human advisor? Make sure the robo-advisor has everything you need.

Can you lose money with a robo-advisor?

Yes, you can lose money with a robo-advisor, just like you can with any investment. While they diversify your investments, there’s nothing saying that you won’t lose some money at some point. Make sure you choose the right portfolio and choose a robo-advisor that automatically rebalances your account.

Do robo-advisors beat the market?

No, robo-advisors generally try to mimic the market but not beat it. Unless you invest in a robo-advisor that uses smart beta techniques, but those advisors typically have high minimum balance requirements.

What are the top advantages of using a robo-advisor?

Robo-advisors offer a variety of benefits including:

Low costs (usually a percentage of assets under management)

Offers tax-efficient investments

Automatically rebalances your portfolios

Ensures your portfolio coincides with your goals and risk tolerance

Which Robo Advisor is Best for Retirees?

So which robo-advisor is best for retirees like yourself? I suggest Personal Capital. It offers the best of both worlds, giving you room for DIY investing with automated investing. You get the bonus of personal finance advice, ensuring that you stay within your guidelines while maximizing your retirement income.

Summary

I like Personal Capital, the platform is truly the best allrounder. Especially if you are a little bit more involved with investing. However if you are the hands-off type investor there are a ton of other choices out there.

Please don’t hesitate to ask any questions and feel free to share your experience with any of the services I wrote about.

Michael is a senior writer at The Robo Investor. He earned his master’s at the Craig Newmark School of Journalism at CUNY, and is currently taking CFP courses at the University of Scranton. He has been an avid finance enthusiast ever since he started investing at the age of 23. Meet the Team

A lot of the big players in the robo advisor niche offer tax-loss harvesting.

In this article I will discuss how tax loss harvesting works, the benefits of automation and which robo advisors I recommend for tax-loss harvesting.

What is Tax Loss Harvesting?